The citizens of the world are having to consider risk in a whole new light as part of the experience of Covid-19.

Risk is synonymous with the prospect of loss and managing risk in the context of investment is an art perfected by advisers. This function has become the most regulated aspect of advice. It is only by building headroom for losses which must be correctly anticipated that the longer-term benefits can be accrued, including allowances made for known knowns and known unknowns. As everybody struggling to adapt to the present circumstances will appreciate, managing risk also involves adjustments. Whatever model you are working to evolves through experience.

Bound up in all the rules and regulation, is a very specific challenge that sits at the heart of modern advice – evidencing the ‘need to take risk’, again, something we are working through as a nation coming out of lockdown – we can’t spend the rest of our lives in perfect infection-free environment, so risk will be part of our lives.

In investment advice, the ‘need to take risk’ is the most important factor in delivering reliable advice and meeting the Suitability requirements. Don’t forget the regulator will rule against an adviser if the client has been exposed to too great a risk, even if he or she may have made greater profits than expected! The adviser does not have the luxury of timing the market or relying on tactical shifts in a client’s investment strategy to generate market returns. Many customers believe that this is a role that advisers perform, but it isn’t. Advisers rely on optimising long-term strategies based on the predicted performance of diversified portfolios. The demise of Woodford has removed much of what was left of the allure of the ‘star manager’. Now it is all about the objective study of the performance of asset classes.

Speculation, more often than not negates the value of regulated advice. Just as a failure to control risk of infection could have catastrophic consequences, explore any failure of advice, and speculation will be at the heart of it, whether it comes in the form of Barbadian resorts, Costa Rican Forestry or slick methods of peer-to-peer lending to start-ups.

A stock-in-trade for advice is the ability to provide the greatest possible certainty of outcome. This is a fascinating challenge best met using probability-based forecasts. The latter can be used to define what the likely outcome will be – and these tend to be very accurate in stochastic models such as Moody’s (formerly Barrie + Hibbert). The benefit of the Moody’s model is that it will provide the likely (and historically accurate) prediction of the outcome of the investment but also the extent of losses than are to expected throughout the term, offered as a ‘Value at Risk’ metric.

Using probability-based analysis, advisers can accurately and reliably align their client’s plans to appropriate investment strategies defined by their risk and return metrics – so the ‘need to take risk’ is clearly understood by the client thus providing ‘informed consent’. Financial plans are therefore achievable and realistic.

We will see that it is very difficult to predict the outcome of an investment in the short term, but longer term, the power of probability kicks in and we can predict outcome much more accurately. It is a similar explanation as to why a dice may have 1 out of 6 outcomes in a throw, meaning the next throw is impossible to predict. However, throw a dice 10k times and the outcome can be predicted with certainty.

Consideration of term

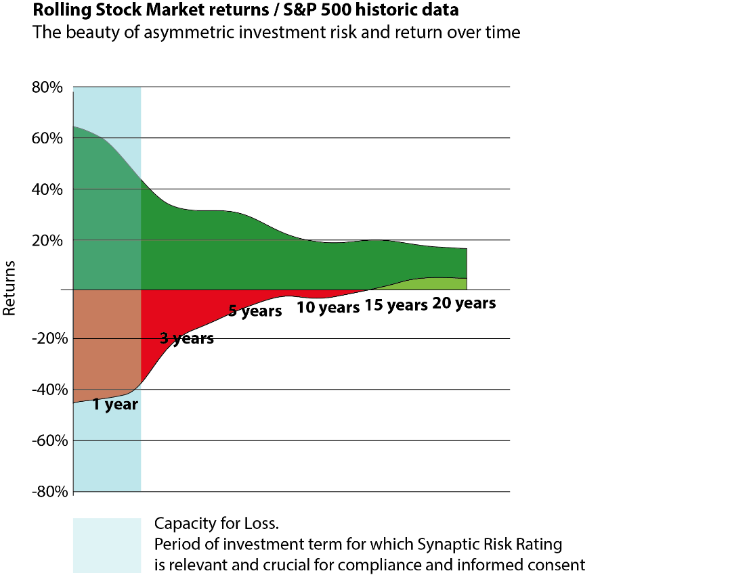

Term changes everything, including Capacity for Loss. The higher the Capacity for Loss, the higher the investment risk a n investor can afford to take. Investment risk diminishes as the term extends, or, as ‘Sequence of Return’ risk is mitigated. In Covid-19 terms, managing the short term risks is the strategy that allows confidence in normal conditions to return.

How does term reduce risk of loss?

Over short time periods, an index such as a FTSE or S&P can deliver exceptionally high or low returns. If we look at the S&P 500, 1973 – 2016, the worst 1 year rolling return was -43% (to month ending February 2009). The best was +61% return (to month ending June 1983).

However, the worst 20 year rolling return was 6.4% (gain, to May 1979). The best rolling 20 year period delivered an average of 18% a year (to March 2000). So: you could argue that if you are going to be invested for 20 years, Capacity for Loss is irrelevant, though of course that is not how compliance works - as an adviser you need to account for the short term as well.

If you would like to learn more about our financial research solutions, please get in touch

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.

Related Articles

What does the FCA say about the use of risk profiling and asset allocation tools?

The FCA’s current emphasis on risk and suitability was firmly established in the key guidance consultation paper FCA GC 11.01 (2011): Assessing suitability: Establishing the risk a custome...

By Eric Armstrong

Client Director, Synaptic Software Limited

- 5 min read

- 26 Jan 2022

What firms need to know about using risk profiling and asset allocation tools

There are several reasons why risk is one of the most difficult areas of financial advice to get right. The purpose of this guide is to walk practitioners, whether financial services comp...

By Eric Armstrong

Client Director, Synaptic Software Limited

- 5 min read

- 19 Jan 2021

The need to take risk

The concept of a recommendation forms the cornerstone of the regulatory framework. Advice is a regulated activity....

By Eric Armstrong

Client Director, Synaptic Software Limited

- 5 min read

- 29 Jan 2021