A most exceptional recovery

Guy Monson, Sarasin & Partners

In this edition...

- A Most Exceptional Recovery Guy Monson, CIO and Senior Partner Sarasin & Partners

- Staying the course Andrew Morris, Product Specialist Canada Life Asset Management

- Price and value: what you pay versus what you get John Husselbee, Head of the Liontrust Multi-Asset investment team Liontrust

- Why rebalancing client portfolios is good practice Georgina Yarwood, Investment Strategy Analyst Vanguard Europe

- Market Timing: is now the time to move your portfolio into cash? Hugo Thompson, Multi-Asset Investment Specialist HSBC Asset Management

- The investment journey: a balancing act Kirsty Wright, Head of Proposition – Pensions & Funds LV=

- Helping mining groups meet the challenge of sustainable development Sandra Crowl, Stewardship Manager Carmignac

- Introducing Multi-Asset Solutions in Goldman Sachs Asset Management Shoqat Bunglawala, Head of Multi-Asset Solutions for EMEA and Asia Pacific Goldman Sachs Asset Management

- What is the post-pandemic outlook for Asian shares? Richard Sennitt, Fund Manager, Asian Equities Schroders

- Retirement should be enjoyed, not endured John Stopford, Co-portfolio Manager, Diversified Income Fund Ninety One

- Is passive investing killing ESG? Jon Lycett, Business Development Manager RSMR

- Emerging from the winter of discontent Salman Ahmed, Global Head of Macro and Strategic Asset Allocation Fidelity International

- IG credit: bubble trouble, alpha opportunity, or both? Adam Darling, Co-manager Jupiter Corporate Bond

- The Unknown King-Makers of ESG Editorial team, Synaptic Software Limited

- How to drive more protection business to your website in 6 easy steps Editorial team, Synaptic Software Limited

- Innovation that protects: Webline journey updates Richard Tailby, Head of Sales Synaptic Software Limited

- Make your Central Investment Proposition (CIP) a pillar of your success Terry Lawson, Business Development Manager Synaptic Software Limited

- The ‘ex-ante’ compliance is icing on the financial planning cake Eric Armstrong, Client Director Synaptic Software Limited

Make your Central Investment Proposition (CIP) a pillar of your success

Terry Lawson

Business Development Manager Synaptic Software Limited

For several years, surveys have indicated that a large proportion of firms work with a CIP. In fact, it would be very hard not to, as the PROD rules designed to support the directives of MiFID II, dictate that investment solutions should be researched and maintained for 'client types', or segments. This requires delivering 'ready-to use' investment solutions as opposed to bespoke systems on a client by client basis. This is an inversion of the approach demanded pre-RDR and MiFID II where 'whole of market' research was required to demonstrate suitability on a 'case-by-case' basis. The purpose of this article is to explain how Synaptic Pathways is the perfect tool to build and maintain a CIP in order to deliver best advice.

The benefits of the CIP are easy to identify:

-

Standardisation

- Creating a CIP (and its offspring CRP (for retirement)) is about configuring optimum investment solutions for repeated use. Obviously, there is flexibility to tailor solutions to individual client needs (as 'a firm must take reasonable steps to ensure a personal recommendation is suitable for each client')1.

- Standardisation is the basis of achieving consistency, without which, quality is harder to maintain and scalability and repeatability are impossible.

- It is easier to review a model inherited by various clients than review multiple disparate investments.

-

Reliability of returns

- A key role of the adviser is to match the goals of the financial plan to an investment strategy whose anticipated returns are predictable (to the extent that they can be).

- It is pointless planning for a future that is completely unknown. Markets can and do perform erratically in the short term where they are capable of large gains or losses, but they tend to conform to known characteristics in the longer term. In the Synaptic Guide to Risk, downloadable from the Synaptic website, we discuss the phenomenon by which market returns become more predictable in the longer term. This is partly how risk models like Moody's Analytics achieve such remarkable accuracy.

-

Compliance

- We know that suitability, in the context of long-term savings and retirement, is the key area of enforcement focus for the FCA who are demanding full suitability assessments to be made as part of client reviews. (Remember that prior to MiFID II, adviser charging on an on-going basis required proof of servicing, NOT proof of suitability as it does now).

- Working with a CIP (and/or CRP) can represent an enormous saving in terms of time and effort, as well as fewer errors. As previously alluded to, the key relationship is between the CIP and a range of clients (identified by segment), rather than multiple, individually researched solutions.

All these benefits are important, irrespective of how big a firm you are. A key difference between a large vertically integrated advice organisation and a small one may be the outsourcing of the investment management. The research requirements remain the same.

FCA Final Guidance 12-16. Assessing suitability: Replacement business and centralised propositions

This was an important document recognising that the adoption of a CIP was an important trend, with firms adapting to the requirements of RDR. As advisers reorganised their businesses in line with the new rules, CIPs allowed them to move from a culture of commission offered by product providers to remuneration by adviser charging, facilitated by investment platforms (including wraps).

The paper underlined, as ever, the importance of suitability and the responsibility of the firm 'to take reasonable steps to ensure the suitability of recommendations to switch any existing investment into a new investment solution'2 in the case of 'replacement business'.

'Key issues firms should consider' included consideration of clients' 'needs and objectives'; collection of 'necessary information' relating to the investment including 'costs' and 'performance'; and 'implement a robust risk-management system to mitigate the risk of unsuitable advice and poor client outcomes'.3

It is the role of research to combine all this information and provide the illustration to demonstrate suitability, creating reports that exceed both compliance and customers' expectations. The risk-management system built into Synaptic research is the stochastically derived framework from Moody's Analytics, the peerless leader of risk analytics in our industry.

The role of research

In maintaining a CIP and delivering advice in a way that is beneficial to firm, adviser and customer, research has a central role to:

- Make the complicated process of maintaining and evidencing a CIP easy.

- Ensure that product and fund governance is embedded in the advice process – including management and use of panels (platform / product / portfolio and fund).

- Identify the appropriate investment solutions that have been configured to align with the needs of specific client types or segments.

- Provide access to charging data at platform, product and portfolio (including DFM) level is how Synaptic adds additional value – multiple look ups and reconciliation are no longer necessary multiple look ups and reconciliation are no longer necessary as they can now be done automatically. MiFID requires all costs to be illustrated (not just fund costs). Synaptic also identifies the correct share class for any given wrapper.

- Provide a consistent methodology for illustrations and disclosure to support recommendations whether on an ex-ante or ex-post basis.

- Risk profile the customer to ensure that their appetite for risk and ability to sustain losses (capacity for loss) are known and documented.

- Demonstrate alignment of a client's investment objectives with an investment strategy represented by the CIP.

- Forecast the investment outcome of the investments to demonstrate the role of risk in acquiring market returns and delivering on financial planning objectives.

- How a firm chooses to configure their CIP should be entirely down to them. The software allows them to capture segments, target market and all other data to reflect their approach to advice.

Good Practice

One firm commissioned the development of a bespoke MI package which the Compliance Director used every day. The MI provided real-time updates for each adviser against a variety of criteria, such as the business mix (including the proportion invested in the CIP), provider mix, product persistency, income levels and file review results. The MI package enabled the Compliance Director to regularly ask each adviser technical questions. Their answers enabled the firm to develop targeted training sessions for the advisors and fed into their ongoing competency assessment.

This extract from FC FG: 12-16.4.29 indicates the extent to which software must capture relevant data, including 'provider mix'. It is not just about funds.

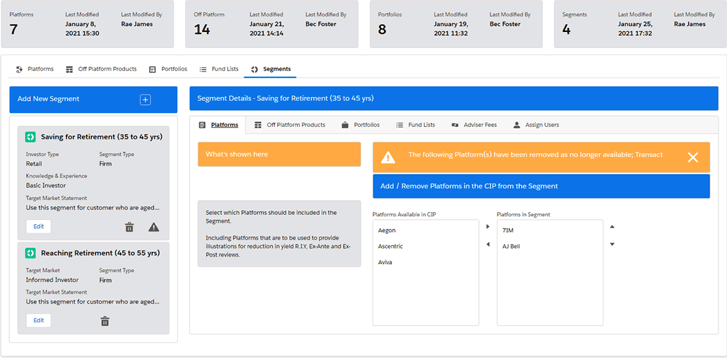

Synaptic screen showing a standard 'CIP' segment with the ability to configure solutions including platforms, products, portfolios and approved funds. There is no more transparent or structured way of working or demonstrating compliance. Only Synaptic can deliver the granularity of platform, product and fund data. Assigning users allows firms to control access to CIP in respect of competency.

Call Synaptic today and ask to see the new CIP management capabilities in the new Synaptic Pathways software.

Call 0800 783 4477 or email hello@synaptic.co.uk

- FCA FG12-16. 4.13

- FCA FG12-16. 3.1.

- FCA FG12-16. 3.3.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.