Few places to hide

Sarasin & Partners

In this edition...

- Hours to minutes Editorial team, Synaptic Software Limited

- Synaptic Pathways: the advice research revolution has arrived Eric Armstrong, Client Director, Synaptic Software Limited

- Value for money matters when assessing suitability John Warby, Senior Business Relationship Manager, Synaptic Software Limited

- The road ahead on suitability and disclosure Natalie Holt, Content Editor The Lang Cat

- Developing your investment proposition David A Norman (DAN), CEO TCF Investment

- State of the Nation Ian McKenna, Founder of Financial Technology Research Centre and AdviserSoftware.com FTRC

- Few places to hide Guy Monson, CIO and Senior Partner Sarasin & Partners

- Ensuring the “new normal” is a better normal Ben Lester, Head of Distribution – UK & International Praemium

- Stay the course if you can (but better too early than too late) James Klempster, Deputy Head of the Liontrust Multi-Asset team Liontrust

- Can financial goals be achieved through one fund? Mohneet Dhir, Multi-Asset Product Specialist Vanguard Europe

- Talking Trash: Why it’s not a waste of time Luke Barrs, Head of Fundamental Equity Client Portfolio Management for EMEA & Asia ex-Japan Goldman Sachs Asset Management

- Demand for growth funds rises amid risk-on environment Antony Champion, Head of Intermediaries Brewin Dolphin

- The best of both worlds Ian Jensen-Humphreys, Portfolio Manager Quilter Investors

- Global Sustainable Equity: a renewable, electric and digital future Hamish Chamberlayne, Head of Global Sustainable Equities | Portfolio Manager Janus Henderson

- Four steps to choose an ESG manager Daniel Ryan, Manager Research Analyst Fidelity International

- The path to retirement is changing … are you? Editorial team, Synaptic Software Limited

- Are unregulated investments ever a good idea? Jon Lycett, Business Development Manager RSMR

- Putting the children first Jacqui Gillies, Marketing and Proposition Director Guardian

- Why not Serious Illness Cover? Nick Telfer, Protection Development Manager VitalityLife

Are unregulated investments ever a good idea?

Jon Lycett

Business Development Manager RSMR

The advice firm involved in the British Steel transfer scandal, Argent Wealth, has been told to pay out after the Financial Ombudsman Service found its advice to steel workers 'insufficiently compelling'; the transfer to leave their defined benefit pension scheme in favour of unregulated investments shouldn't have gone ahead.

"There's been little emphasis placed on financial literacy in schools, but there is now a move towards making the younger generation more financially savvy. The lack of basic investment knowledge means that the get-rich-quick schemes capture the imagination."

Stories like this just keep on coming. What's the engagement history for financial advice in the UK and what effect do shocking tales like these have on the public's approach to this advice? Historically, we have low levels of engagement in the UK with few people seeking financial advice. Thanks to these stories, the profession has not always had a convincing reputation.

Research reveals that a fifth of Brits have no pension savings at all and only 9% of UK adults consult a financial adviser. Given that half of all Britons hope for a retirement income of £20k+ per year and the current maximum state pension is £9,110, there's a gaping disparity between people's expectations and reality. Seeing a financial adviser would be an obvious way of meeting this objective but relatively few people go down this route due to an ingrained lack of trust. The tide is slowly turning though, with proof of the professionalism and credibility of such advice making more people consider consulting advisers to plan their future.

Where are we at when it comes to financial education? There's been little emphasis placed on financial literacy in schools, but there is now a move towards making the younger generation more financially savvy. The lack of basic investment knowledge means that the get-rich-quick schemes capture the imagination. The first step on the property ladder is relatively unattainable so the younger generation is always playing catch up. First-time investors often associate investing with gambling, choosing to put their money into higher risk investments such as cryptocurrency and fast-moving individual shares. More basic education is needed on longer-term investing to pave the way to a more informed future.

How do we tackle the issue of advisers and organisations cheating people and the damage caused? Bad news travels fast and folklore can create a general mistrust of the industry. Financial advisers are generally fined or barred but there's no criminal conviction associated with bad advice. The FCA says that unregulated investments can be used for sophisticated or high net worth investors. Not all instruments are appropriate for all clients and there can be a lack of understanding and provision of sound advice when it comes to these products. Why are there unregulated investments? If advisers use unregulated investments inappropriately, the investor is exposed. People need to be protected, sometimes from themselves.

The FCA has urged several thousand people who are clients of liquidated IFA firms to seek compensation over pension transfers. The Financial Services Compensation Scheme (FSCS) is funded by a levy made up of financial advisers in the UK, the vast majority of whom are genuine, hardworking people who are paying through the nose to fund the compensation claims of a small percentage of adviser firms that aren't behaving honestly. The annual figure that the FSCS pays out to clients of firms that went bust keeps on rising. According to the lifeboat scheme's annual report for 2020/21, £584m was awarded to consumers, a £57m increase from the previous financial year. So not only do we have a mistrust of the industry, we now have an industry that's shrinking due to the expense of funding a levy that pays for the bad advisers.

Incredibly, some former advisers that have gone into liquidation have been able to start claims' management companies. An adviser can effectively mis-sell pension advice, set up a claims' management company in their partner's name, sue their former business and gain a fee through the dodgy advice that they gave in the first place. Fraud is classed as a criminal offence, so why isn't this? A few bad pennies can damage the reputation of advisers and financial advice companies across the board and confidence in the industry would likely improve if there's discouragement for dishonest individuals. So, what's to be done?

Technology could offer a solution. Four Eyes Financial is a compliance platform that allows the Canadian regulator to have a live view of client files. The FCA needs to be more on the front foot and could achieve that by using this type of technology. If advisers want to use unregulated investments, how about more exams and more scrutiny? And if they're found using unregulated investments when they shouldn't be or aren't qualified to, it's a criminal offence? Stopping advisers from using unregulated investments altogether could successfully close the existing loopholes that lead to bad advice. Google has recently announced a policy change meaning that it will only run ads for financial products and services where the advertiser has been verified by the FCA. Digital regulation is a move in the right direction, now it's down to the FCA and their ability to police a system.

The financial industry has had a professional make-over during the last decade but trust and engagement can only truly start to flourish when the industry gets its own house in order, creating a world where investors can have faith in the advice profession and honest advisers no longer have to cover the costs of unscrupulous ones.

Investing isn't gambling, it's having an objective and an understanding of how long you need to get to that long-term goal. RSMR supports advisers who are committed to financial planning rather than chasing fast returns. Our research is rigorous, allowing advisers to set considered plans and objectives. All the funds that we rate are regulated and listed within an Investment Association sector, so our starting point is robust and then refined by us.

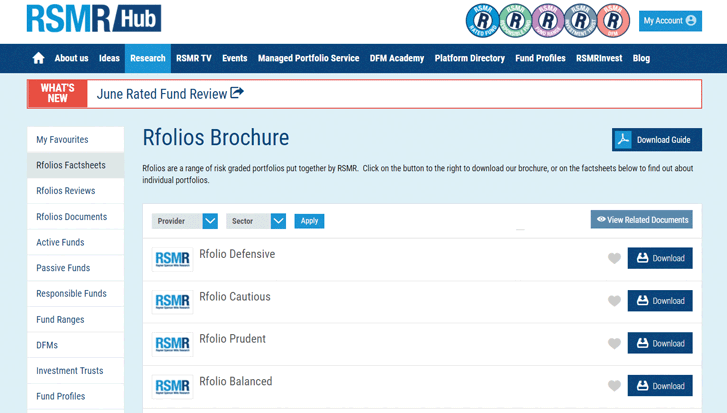

Would you like to find out more about our in depth, qualitative, forward-looking research? The RSMR Hub is a FREE service offering financial professionals investment solutions and the very latest content, including ratings, fund profiles, factsheets, insights, market updates and event information.

If you’d like to find out more about how RSMR can help shape your client proposition, head to www.rsmr.co.uk

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.