Few places to hide

Sarasin & Partners

In this edition...

- Hours to minutes Editorial team, Synaptic Software Limited

- Synaptic Pathways: the advice research revolution has arrived Eric Armstrong, Client Director, Synaptic Software Limited

- Value for money matters when assessing suitability John Warby, Senior Business Relationship Manager, Synaptic Software Limited

- The road ahead on suitability and disclosure Natalie Holt, Content Editor The Lang Cat

- Developing your investment proposition David A Norman (DAN), CEO TCF Investment

- State of the Nation Ian McKenna, Founder of Financial Technology Research Centre and AdviserSoftware.com FTRC

- Few places to hide Guy Monson, CIO and Senior Partner Sarasin & Partners

- Ensuring the “new normal” is a better normal Ben Lester, Head of Distribution – UK & International Praemium

- Stay the course if you can (but better too early than too late) James Klempster, Deputy Head of the Liontrust Multi-Asset team Liontrust

- Can financial goals be achieved through one fund? Mohneet Dhir, Multi-Asset Product Specialist Vanguard Europe

- Talking Trash: Why it’s not a waste of time Luke Barrs, Head of Fundamental Equity Client Portfolio Management for EMEA & Asia ex-Japan Goldman Sachs Asset Management

- Demand for growth funds rises amid risk-on environment Antony Champion, Head of Intermediaries Brewin Dolphin

- The best of both worlds Ian Jensen-Humphreys, Portfolio Manager Quilter Investors

- Global Sustainable Equity: a renewable, electric and digital future Hamish Chamberlayne, Head of Global Sustainable Equities | Portfolio Manager Janus Henderson

- Four steps to choose an ESG manager Daniel Ryan, Manager Research Analyst Fidelity International

- The path to retirement is changing … are you? Editorial team, Synaptic Software Limited

- Are unregulated investments ever a good idea? Jon Lycett, Business Development Manager RSMR

- Putting the children first Jacqui Gillies, Marketing and Proposition Director Guardian

- Why not Serious Illness Cover? Nick Telfer, Protection Development Manager VitalityLife

Developing your investment proposition

David A Norman (DAN)

CEO TCF Investment

This is the first in a series providing ideas and thoughts for IFAs looking to design, build, or run a Centralised Investment Proposition (CIP) or Centralised Retirement Proposition (CRP).

"Thinking about your firm and its background, the intermediaries that you work with and the type of clients you have, or are targeting, will impact the design of your CIP/CRP."

It is based on the author's own experiences of working with over 150 firms who have sought ideas, input, and challenge to their current processes. Whilst it should not be considered formal compliance advice we hope you will find it useful.

The foundations

The FCA referred to CIPs in the finalised guidance issued in July 2012 'Assessing suitability – replacement business and centralised investment propositions1.' It is still an excellent starting point for those looking to create a CIP and provides some examples of good and poor practice to draw from.

With the advent of Pensions Freedoms, several adviser firms started to look at whether they needed to update their CIPs for "drawdown" clients, and so CRPs were born.

The combination of Pensions Freedoms and the ageing UK population has also prompted more interest from the Financial Conduct Authority (FCA) into how the retirement market operates. This interest was flagged in the FCA 2019 Sector Review paper:

"Some adviser firms have not yet updated their investment strategies for decumulation clients. In addition, they may not have adequately considered decumulation risks2."

Key areas3 that the FCA suggested advisers need to be aware of included:

- You need to ensure the advice you provide is suitable, costs and charges are disclosed clearly, and you act in the best interests of your clients.

- Conflicts of interest must be identified and where they cannot be prevented, disclosed, and managed.

- Inadequate fact finding creates a high risk that your advice will be unsuitable.

Putting this into practice

Many firms initially think of a CIP / CRP as a standalone compliance document that articulates how they design investment solutions for clients. But this is only part of the picture. A CIP / CRP is more likely to be the description of the end-to-end processes, thinking and evidence that underpins and articulates your investment solution. It may well include a document that articulates your investment beliefs (your Investment Philosophy and Process).

Most firms that we have worked with end up with a few short documents rather than one long tome. They typically include a simple client facing document that can be used to show the value of the process to customers. In addition to this a firm will then have a set of internal documents / checklists that describe the processes to ensure it is delivering consistent good outcomes. They will also have the evidence and management information to validate these processes.

Some firms have simple CIP / CRPs as they deal with only a few core segments. Others have more detailed documentation that is used by a larger adviser team, to ensure consistent recommendations / outcomes, and to facilitate / evidence senior management monitoring.

Thinking about your firm and its background, the intermediaries that you work with and the type of clients you have, or are targeting, will impact the design of your CIP / CRP. The way you articulate your Investment Proposition, and indeed what are appropriate instruments, may be different if you deal with high-net-worth entrepreneurs or if you only deal with elderly clients with modest means. The FCA wants to see the evidence and research that you have conducted to underpin your processes and recommendations – this is particularly true with CRP (the decumulation phase).

But it is always worth keeping it as simple as possible (and that takes time)!

Is a CIP/CRP mandatory?

In short, the answer is no. But you MUST be able to DEMONSTRATE why and how:

- You have assessed the detailed hard and soft facts for customers.

- Your recommendation meets the needs of your specific client segments.

- Solutions are suitable for accumulation or decumulation clients.

- The assumptions in your process are robust and reliable (evidence).

- You manage conflicts of interest.

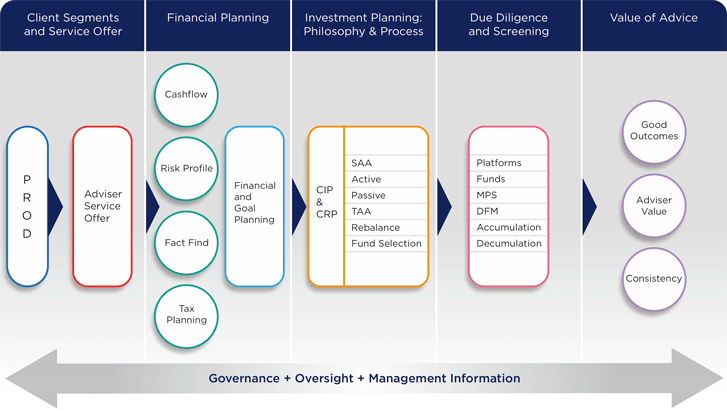

Below is a simple diagram that we have used with firms to show how the elements of a CIP / CRP may fit together:

- What are your customer segments, what are their characteristics / needs?

- What service offer would best serve their needs on a profitable basis?

- How do you collect the facts (hard and soft) and risk information for your recommendations?

- Do you use a cash flow modelling tool (and what are the assumptions within it)?

- What investment views do you hold? What data / evidence / assumptions underpin these? How do you manage the different risks in accumulation and decumulation? How do you manage any potential conflict of interest?

- How do you incorporate the customer segmentation needs into your due diligence? What are the key scoring criteria?

- What oversight and monitoring do you have of your processes?

- How do you show the value of all this work to your clients?

- And this all needs to be underpinned by governance and monitoring – are you getting the expected outcomes / do you need to update your assumptions / solutions?

"Do not forget it is your clients' needs and your service proposition that will determine good outcomes."

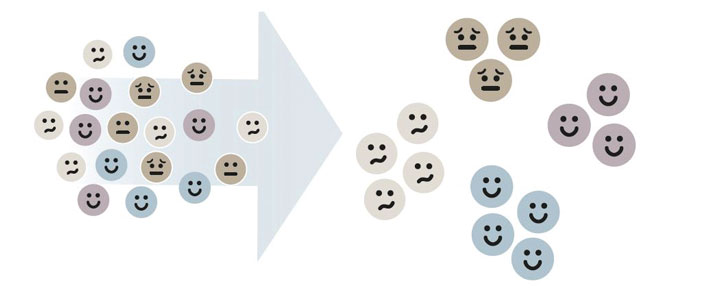

Segmentation – who is it for?

Before you can design your CIP / CRP you need to understand your broad client segments. There is no prescriptive / right way of doing this. We have seen firms use asset size, life stage and service proposition.

Life stage is becoming the most common: young clients need a growth / accumulation proposition, mature clients may need steady income / preservation solutions, elderly clients may need maximum income solutions.

Asset value is more difficult to justify as an appropriate segmentation method. While smaller value clients may benefit from an all-inclusive service offered by a fund of funds solution – it is harder to justify why young savers with £25,000, would need the same outcome as a retired widow with £25,000 to invest.

And while the investment solution that you use (insourced or outsourced) may vary, it is again difficult to see how this can be used to differentiate clients – that is your offer, not a client attribute.

Areas to reflect on are likely to be client life stage, family group, overall objectives, level of experience, complexity of needs and overall wealth.

What is clearly emerging is that advisors are tailoring their advice service and the investment solution included therein to different client segments:

Ensuring you have a clear approach for each segment designed to deliver a good outcome is what matters. And this is growing in importance post Pensions Freedoms – the "saving up" and "drawing down" stages will require different thinking and approaches.

The PROD rules were introduced as part of MiFID II in 2018. So, if you have not documented and implemented PROD you need to get your skates on! There is no right answer to how you should create / document your segmentation, but your back office / CRM system is a good place to start.

Do not forget your service offer

One area that has emerged many times from the work we have conducted with adviser firms is, that once the PROD segmentation has been completed, they look at their current service offer and realise that it does not really meet different client needs.

The post RDR typical offer of gold, silver, and bronze service (typically by asset value) no longer fits. Whereas an 'accumulation', 'transition to retirement', 'decumulation' and 'later life' set of services more closely meets typical client needs. For example, a younger client's need for cash flow modelling is typically less sophisticated than one needed for people retiring today. Think Lager, Aga, Saga, and Gaga as Annie Tempest caricatures.

Do not forget it is your clients' needs and your service proposition that will determine good outcomes. If you wish to offer a service that only certain platforms can accommodate then that would be a reason for excluding those that cannot (e.g., regular income payments from multiple model portfolios in drawdown).

TCF Investment have developed a range of different templates that might help IFAs with CIP / CRP development.

Source:

- https://www.fca.org.uk/firms/assessing-suitability

- https://www.fca.org.uk/publication/corporate/sector-views-january-2019.pdf

- https://www.fca.org.uk/publication/correspondence/portfolio-strategy-letter-for-financial-advisers.pdf

Disclaimer:

This publication has been produced by TCF Fund managers LLP (TCF). It is provided to UK authorised financial advisers for information purposes only, and TCF makes no express or implied warranty, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included in this publication. TCF accepts no liability for use of this report and advisers should seek their own specific compliance or other professional advice.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.