A most exceptional recovery

Guy Monson, Sarasin & Partners

In this edition...

- A Most Exceptional Recovery Guy Monson, CIO and Senior Partner Sarasin & Partners

- Staying the course Andrew Morris, Product Specialist Canada Life Asset Management

- Price and value: what you pay versus what you get John Husselbee, Head of the Liontrust Multi-Asset investment team Liontrust

- Why rebalancing client portfolios is good practice Georgina Yarwood, Investment Strategy Analyst Vanguard Europe

- Market Timing: is now the time to move your portfolio into cash? Hugo Thompson, Multi-Asset Investment Specialist HSBC Asset Management

- The investment journey: a balancing act Kirsty Wright, Head of Proposition – Pensions & Funds LV=

- Helping mining groups meet the challenge of sustainable development Sandra Crowl, Stewardship Manager Carmignac

- Introducing Multi-Asset Solutions in Goldman Sachs Asset Management Shoqat Bunglawala, Head of Multi-Asset Solutions for EMEA and Asia Pacific Goldman Sachs Asset Management

- What is the post-pandemic outlook for Asian shares? Richard Sennitt, Fund Manager, Asian Equities Schroders

- Retirement should be enjoyed, not endured John Stopford, Co-portfolio Manager, Diversified Income Fund Ninety One

- Is passive investing killing ESG? Jon Lycett, Business Development Manager RSMR

- Emerging from the winter of discontent Salman Ahmed, Global Head of Macro and Strategic Asset Allocation Fidelity International

- IG credit: bubble trouble, alpha opportunity, or both? Adam Darling, Co-manager Jupiter Corporate Bond

- The Unknown King-Makers of ESG Editorial team, Synaptic Software Limited

- How to drive more protection business to your website in 6 easy steps Editorial team, Synaptic Software Limited

- Innovation that protects: Webline journey updates Richard Tailby, Head of Sales Synaptic Software Limited

- Make your Central Investment Proposition (CIP) a pillar of your success Terry Lawson, Business Development Manager Synaptic Software Limited

- The ‘ex-ante’ compliance is icing on the financial planning cake Eric Armstrong, Client Director Synaptic Software Limited

The Unknown King-Makers of ESG

Editorial team

Synaptic Software Limited

In the aftermath of the global financial crisis, we learned several lessons. We learned that the big banks can commit crimes that take us to the brink of financial collapse, and then when forced into a settlement can actually craft such a settlement in a way that allows for partial taxdeductibility of the ensuing penalty, thereby shifting the cost to taxpayers through lost tax revenues.1

"We learned that the big banks can commit crimes that take us to the brink of financial collapse."

We learned that in times of stress, the Federal Reserve will actually pay interest on required reserves, essentially paying banks to be banks, and ensuring that they hoard as much cash as they can in an interest-bearing safe-haven; the absolute antithesis of what they were meant to be doing to 'unfreeze' the economy and spur lending.2

We learned that when all else fails, the government will take over the two largest mortgage lenders in the world's largest economy, and then turn around and remove any and all fiscal restraints on their credit lines, thereby allowing the holders of toxic assets to dump everything on taxpayers at vastly inflated prices.3

We also learned that, beyond the attention-grabbing, bile-inducing headlines above, there were unassuming, yet manifestly pivotal, players at work that no-one gave a second thought to until the world went to hell in a hand basket – the credit rating agencies. The vast panoply of mislabelled assets holding themselves out as 'investment grade' that were bundled, packaged and foisted on investors only held gravitas because these known and trusted agencies had given them the 'Good Housekeeping Seal of Approval'.

An enormous swath of financial detritus could be bundled together, boxed up and sold at a premium, because the buyer trusted the rating agency such that when they wrote 'diamonds' on the box, it meant the box actually contained diamonds. That notion now seems quaint and naïve in retrospect, but it was the prevailing thinking of the time. The point of referencing the above is that these often overlooked, mundane 'checks and balances' are absolutely key to understanding what is really going in. These under-the-radar providers of services that form the basic building blocks of all that we do carry enormous sway over how and where we invest.

Such is the case with index providers, and in this case how index providers derive their ESG index products. There appears to be a prevailing misconception in the market that an ESG index is one that simply screens for so-called 'sin stocks', and can then simply kick out stocks and sectors it doesn't like and craft a portfolio safe in the knowledge that it passes muster.

The reality is very different. There are several types of index that can be referenced by investors when implementing an ESG investment policy, and it is crucial to understand the various types of index in order to ascertain which best suits the goals we are trying to achieve in this area. While the following is based upon the MSCI family of indices, there are several others out there with their own methodologies.

Becoming the de facto standard for funds is a huge and therefore lucrative business, and so competition is inevitable.

However, given space (and attention span) constraints, we'll stick to just a brief overview of the MSCI offerings, given their market prevalence.

The first category to be aware of is that of an integration index. This type of index seeks to incorporate ESG considerations into its methodology, and leverages upon the existing broad market index products by seeking to enhance exposure to companies with strong sustainability profiles.

In the case of the MSCI Leaders indices, for example, this is done by taking companies that have the highest ESG ratings but with a limit on a sector basis of the top 50% of market cap within their respective sector. This serves to limit systematic risk by pinning the ESG variant to its parent index through its use of sector weights reflective of the parent index. The MSCI Focus index series instead uses an explicit tracking error constraint to maintain adherence to parent weightings, while yet another variant, the MSCI ESG Universal index limits those stocks it explicitly excludes to only the most egregious cases where their activities are "found to be in violation of international norms (for example, facing very severe controversies related to human rights, labour rights or the environment) and companies involved in controversial weapons (landmines, cluster munitions, depleted uranium, and biological and chemical weapons)".

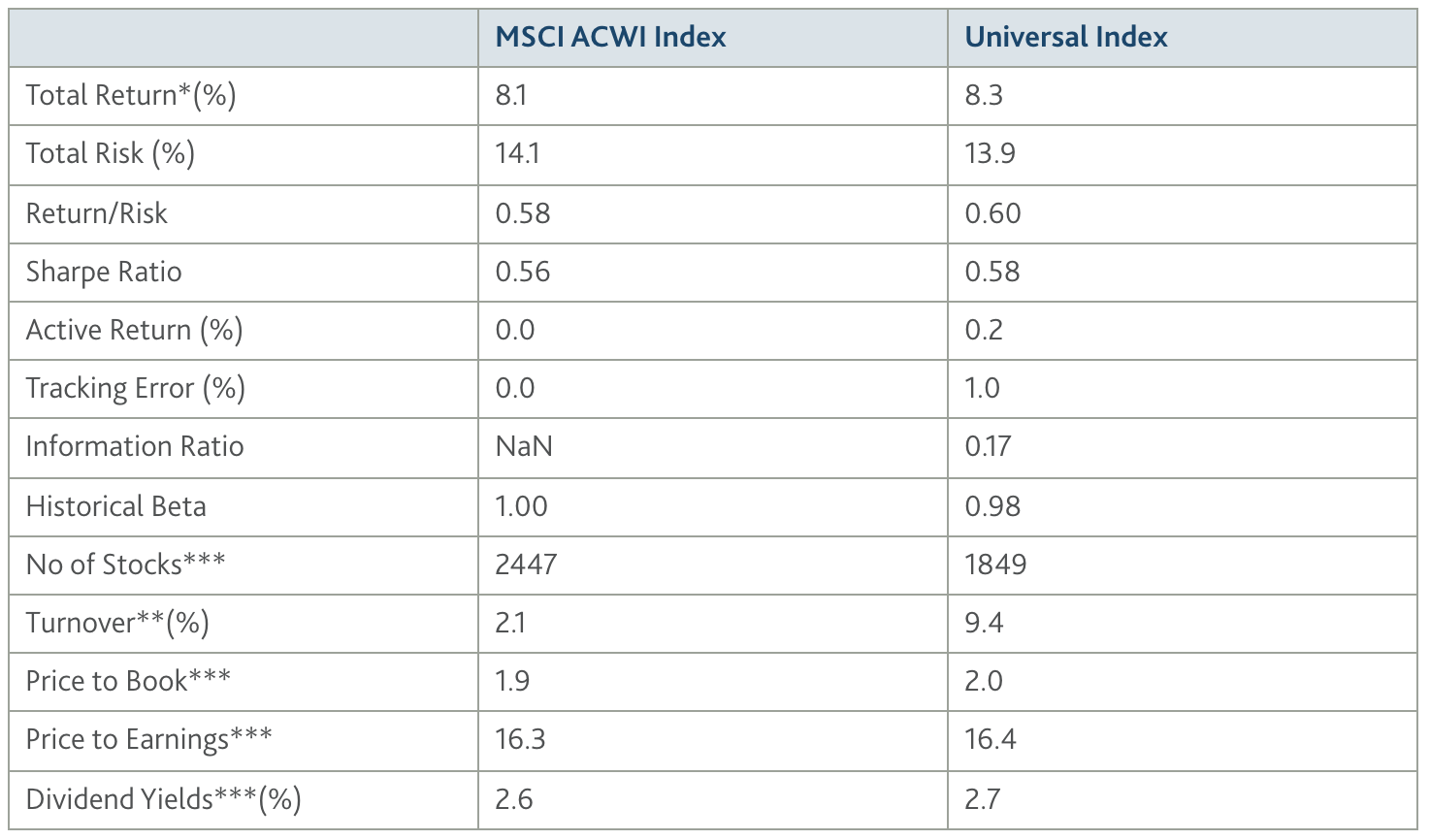

This index series then tilts the portfolio away from its free float weighted parent, seeking to gain exposure to companies with both a higher ESG rating and a positive ESG trend. This is perhaps the one that most deviates from the parent in terms of sector exposures, yet the MSCI back test table shown here demonstrates that such an approach enhances returns, reduces risk, and therefore leads to superior risk-adjusted performance.

The second broad category of index is that of values-based investing. Such indices seek to align the investment portfolio with a given investor's ethical, political or religious values.

Some of these are explicitly exclusionary (in areas such as fossil fuels, tobacco products and controversial weapons), but this category also covers such areas as Socially Responsible Investing (SRI) and faith-based investing (predominantly Catholic or Islamic values).

The third broad category is that of impact investing. Indices in this category seek a more inclusionary approach, deliberately identifying those companies whose core business seeks to address a major social or environmental issue, as defined by the United Nations Sustainable Development Goals4, typically in areas such as sustainable impact, women's leadership and global environment.

We can see, then, that the choice of underlying benchmark is a key consideration for investors in ensuring that their ESG investing falls at a point on the ESG spectrum that is in keeping with their values and desires, both personally and financially. Providers of these indices wield enormous power in shaping the investable universe for trillions of pounds of assets globally, so it's our hope that this quick primer will aid in better evaluating the role that a benchmark index plays in shaping our investment choices.

Period: 30-Nov-2009 to 30-Sep-2016

*Gross returns annualised in USD

** Annualised one-way index turnover over index since 26th Nov 2014

*** Monthly averages

To find out more, call us on 01922 472226, email enquiries@ebi.co.uk or visit www.ebi.co.uk

Works Cited

- Wood, Robert W. Forbes. [Online] September 16, 2014. Web Source

- Board of Governors of the Federal Reserve. Press Release. Federal Reserve. October 6, 2008. Web Source

- Reuters. Treasury uncaps credit ;line for Fannie, Freddie. December 24, 2009. Web Source

- United Nations Department of Economic and Social Affairs. United Nations. Web Source

Past performance is not a reliable indicator of future results. The value of investments, and the income from them may fall or rise and investors may get back less than they invested.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.