Investing in the age of AI

Connections Magazine Q3 2025

In this edition...

- Investing in the Age of AI: Navigating the Opportunity and the Risk Katie Sykes , Senior Marketing Manager - RSMR

- The great wealth transfer Justine Randall, Chief Commercial Officer - Tatton

- The hidden cost of ‘pound-cost ravaging’ for retirees Antony Champion, Managing Director - Head of Intermediaries RBC Brewin Dolphin

- Is the 60/40 Portfolio still working? Jennie Byun, Head of UK Multi-Asset Investment Specialists - HSBC Asset Management

- Multi-asset investing in 2025: from product to partnership James Giblin, Fund Manager - L&G

- What does the US dollar’s recent weakness mean for multi-asset investors? Madison McCall, Multi-Asset Product Management Specialist - Vanguard Europe

- Reports of ESG’s death are greatly exaggerated Jonathan Simpson, Investment Oversight Analyst - ebi Portfolios

- Ten Years of Freedoms – Lessons, Gaps, and the Road Ahead Matt Ward, Communications Director - AKG Financial Analytics Ltd

- Why the UK Needs Better Education on Tax-Advantaged Investments Harry Morrison, Investment Analyst & Panel Consultant - MICAP

- Two years of Consumer Duty: The best of times, or the worst of times? Sandy McGregor, Director of Policy - Simplybiz

- Client Led, Data Driven Paul Bruns, Compliance Director - Simplybiz

- Should estate planning & will writing be part of your offering? Chloe Faulkner, Business Development Manager - APS Legal Associates

- What if your CRM wasn’t just a bit of software? Abi Hortin, Marketing Executive - Plannr Technologies Limited

- Redefining Fintech Solutions Sandy Newman, Director - ifaDASH

The hidden cost of ‘pound-cost ravaging’ for retirees

Antony Champion

Managing Director - Head of Intermediaries RBC Brewin Dolphin

Having spent years working hard and saving carefully to build long-term financial security, retirement marks the start of the decumulation phase - a time to transition from growing wealth to using it to support the life a client has always envisioned.

Having spent years working hard and saving carefully to build long-term financial security, retirement marks the start of the decumulation phase - a time to transition from growing wealth to using it to support the life a client has always envisioned.

Yet actions taken in the first few years of retirement can have an outsized impact on how long money lasts, potentially undermining financial security.

Even with careful consideration of factors such as longevity and inflation, it’s easy to get caught out by negative pound-cost averaging, or ‘pound-cost ravaging.’ This occurs when larger portions of investments need to be sold to maintain a steady income during times when markets are falling. This can reduce the overall value of investments more quickly.

With various income sources available, such as a general investment account, self-invested personal pension, ISAs, offshore bonds and more, understanding where to draw funds from is a key part of ongoing discussions.

Understanding pound-cost ravaging

Many will probably have benefited from pound-cost averaging during their working life – the strategy of investing regularly regardless of market conditions.

This helps to smooth out market volatility.

Pound-cost ravaging, on the other hand, occurs when funds are withdrawn from an investment portfolio during a market downturn. Since investments are worth less, more units need to be sold to generate the same level of income. Those extra sales crystallise losses that might otherwise have been recovered if left untouched. If this happens early in retirement, there’s also a compounding effect, with less capital available in the portfolio to benefit from growth over time.

This erosion can be especially harmful in the early years of retirement, when the investment horizon still stretches decades ahead.

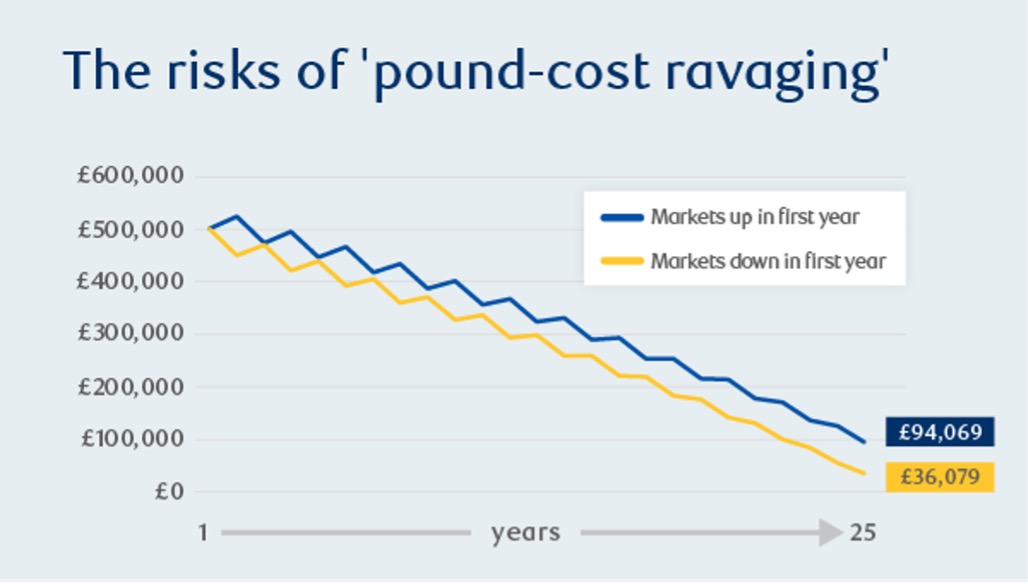

The following chart illustrates the impact pound-cost ravaging can have on a retirement portfolio, revealing the remaining value of a £500,000 portfolio after 25 years of 5% annual withdrawals, depending on whether markets rose or fell in the first year.

First year up: Assumes markets rise 10% and fall 5% in alternating years over 25 years – averaging out at an annual return of 5.23%, net of any costs or investment fees, and making 5% withdrawals of the original sum every year (£12,500). First year down: Assumes the same scenario but markets drop by 5%, following the same pattern of rising 10% and falling 5% in subsequent years over 25 years. Source: RBC Brewin Dolphin.

The effects of pound-cost ravaging can subtly impact even the healthiest portfolios.

Avoiding the pitfalls

Pound-cost ravaging is not the only factor to consider when planning retirement spending. Overestimating investment returns, underestimating longevity, or ignoring inflation can all have long-term consequences, while failing to account for unexpected expenses such as healthcare, family support or home repairs and renovations could also leave finances strained.

On the other hand, some retirees become overly frugal, fearful of running out of money, and fail to fully enjoy the savings they worked so hard to accumulate.

Striking the right balance involves having a clear sense of purpose and a financial plan to match. To avoid pound-cost ravaging, it’s wise to keep an eye on markets and avoid sticking too rigidly to a fixed withdrawal plan. While consistency can feel reassuring, in retirement, flexibility is also key. Setting aside a cash reserve to help adapt spending year by year can extend the life of savings without meaningfully compromising lifestyle needs.

Delaying retirement may be another option, deferring state pension payments, or using other income sources where possible, before tapping into investments.

All these options could give a portfolio more time to grow by avoiding the need to make withdrawals during volatile periods.

An illustrative example

To see how this works in practice, consider Sarah and David, a recently retired couple in their late 60s.

With a combined portfolio of £1.5 million, they were in a strong financial position. Sarah dreamed of travelling more and exploring new destinations, while David looked forward to a quieter life with plenty of time for golf and gardening. They also hoped to support their grandchildren’s education and leave a meaningful legacy for their children.

While they had put themselves in a good position through a lifetime of saving, the couple were aware that managing their money in retirement would require different thinking from how they had built it. With the help of their financial adviser and investment manager, they mapped a financial plan tailored to their long-term goals, factoring in inflation and market fluctuations.

• Protecting against volatility: One of the first concepts their advisers explained was pound-cost ravaging – the risk of depleting investments faster by withdrawing funds during market downturns. To protect their nest egg from market volatility, they decided to set aside two years’ worth of expenses in cash – enough to weather market downturns without touching their core investments.

They also adopted a flexible withdrawal strategy. In years when markets performed well, they withdrew a little more to fund Sarah’s travel adventures; while in leaner years they lived more modestly, drawing on their cash reserve instead of core investments.

• Diversifying for stability: To further protect their finances, their portfolio was allocated across a range of assets, from equities to bonds and alternatives, to spread risk and reduce volatility.

• Planning for the future: Beyond managing their day-to-day spending, Sarah and David worked with their advisers to establish a trust and refine their estate plan so they would leave a financial legacy for their family.

These decisions not only helped safeguard their lifestyle but gave them confidence to enjoy their retirement years.

At RBC Brewin Dolphin, our wealth managers partner with financial advisers to develop tailored strategies for their clients. Together, we help clients achieve a financially secure retirement and greater peace of mind.

Get in touch:

brewin.co.uk/intermediaries

020 3504 7595

salesupport@brewin.co.uk

Important information: The value of investments can fall and you may get back less than you invested. This does not constitute tax or legal advice. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future. Information is provided only as an example and is not a recommendation to pursue a particular strategy. Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness.

RBC Brewin Dolphin is a trading name of RBC Europe Limited. RBC Europe Limited is registered in England and Wales No. 995939. Registered Address: 100 Bishopsgate, London EC2N 4AA. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.