The Final Frontier

of automated (ex-post) reviews conquered

In this edition...

- The final frontier of research and due diligence conquered Eric Armstrong, Client Director

- Hours to minutes Eric Armstrong, Client Director

- World Economic and Market Outlook Graham O’Neill, Senior Investment Consultant, RSM.

- Inflation – what to make of the current dynamics Maria Municchi, Fund Manager, Sustainable Multi Asset Fund Range M&G Investments

- Sustainable Investing – advice from an old hand Hugo Thompson, Multi-Asset Investment Specialist HSBC Asset Management

- The biggest changes in ESG investing over the last 10 years Mark Coles, Head of Nationals & Networks Tilney Smith & Williamson

- Don’t try and defy gravity Catriona McInally, Business Development Manager – Investments Prudential

- Sustainable investing – the defining decades Hamish Chamberlayne, Head of Global Sustainable Equities | Portfolio Manager Janus Henderson

- Finding diversification beyond commercial property Shayan Ratnasingam, Investment Manager Liontrust Multi-Asset team

- Looking to alternatives in an uncertain world Chris Forgan, Portfolio Manager Fidelity Multi Asset

- Developing your investment proposition (CIP or CRP) David A Norman (DAN), CEO, TCF Investment

- Intergenerational Financial Planning Gareth Davies, Pension Specialist, Scottish Widows

- Is your online client reporting up to scratch? Natalie Holt, Content Editor, The Lang Cat

- Partnering here to stay as multi-asset solutions grow Antony Champion, Head of Intermediaries, Brewin Dolphin

- How to Capitalise on the Economic Recovery, Including Morningstar’s Portfolio Positioning Leslie Alba, Associate Director, Research Morningstar Investment Management Europe

- Unemployment insurance is back Kesh Thukaram, Co-Founder Best Insurance

Developing your investment proposition (CIP or CRP)

David A Norman (DAN)

CEO, TCF Investment

This is the second in the series of articles providing ideas and thoughts for advisers looking to design, build, or run a Centralised Investment Proposition (CIP) or Centralised Retirement Proposition (CRP).

"The key for adviser firms is to be able to evidence their beliefs. The importance of costs, the key role that asset allocation plays in long-term returns, and the fact that diversification helps deliver a better risk adjusted return, might feature."

This article looks at data requirements, thoughts on risk and cash flow tools, and elements of an Investment Philosophy and Process.

The data

The FCA guidance has made it clear that the risks in accumulation and decumulation are different. So, if you have not updated your fact find since 2015 then it is unlikely to be fit for purpose.

It is essential that you are collecting a sufficient range of hard and soft facts and that you have explored (and recorded) in detail the retirement income needs of your clients. The most recent FCA Guidance on DB Transfers FG21/3 especially chapter 4 is worth a read (even if you don't advise on DB transfers).

A file note that a client requires "flexible income" is insufficient. What flexibility, over what period, what about later life, what about spouse/partner income, what about escalation/level of guarantees? All these factors need exploration.

The FCA also expects the adviser to challenge the customer; to ensure full understanding, to not just be an order taker, to explain both the advantages and disadvantages of any recommendation.

It is also becoming clear that a full assessment of "essential living costs" and "discretionary spend" is required as the way these are provided e.g., part annuity, part drawdown is potentially different.

Risk tools and assumptions

It is the advisers' responsibility to ensure that the asset allocation generated by a risk profiling tool is appropriate for clients.

The assumptions used by most optimisers are based on some form of historic data. These may be adjusted for expected future returns to make them more forward looking rather than just backward facing. You will need to understand and document these assumptions. Any investment committee would wish to sense check these assumptions, as the data that is used as inputs to these tools is critical to the output. Small changes to long-term return assumptions can make substantial changes to the asset allocation for a given risk profile.

It is also important that advisers understand whether the optimiser return outputs are real (after inflation) or nominal.

Cash flow models and assumptions

The FCA proposed reforms to how cash flow modelling should be conducted for DB transfer cases based on the shortcomings it saw. These are worthy of consideration for wider retirement planning (extract below):

"Firms must prepare cash flow models in real terms, i.e., in today's money terms. This will ensure that the models are consistent with other mandated documents such as Key Features Illustrations.

Firms must ensure that tax bands and tax limits are set using reasonable assumptions if they model net income from year to year. The use of real terms' modelling should facilitate appropriate indexation.

The modelling must include 'stress testing' scenarios to illustrate the impact of less favourable future scenarios, so that the consumer can see more than one potential outcome."1

Even small changes to long-term assumptions within a model will considerably change the outcomes. Advisers need to be alert to this risk and to the potential conflict it creates. Using relatively high future return assumptions could convince clients to move away from an occupational scheme, or to move into drawdown rather than annuitise, when lower returns may not.

It is also perhaps sensible to show clients, especially when entering drawdown, the impact of low/negative returns in the early years and/or the risk of taking high income in the early years. The FCA expects that advisers show the advantages and disadvantages of any proposed solutions – this would be a good way to do so.

As the adage says, "Rubbish In, Rubbish Out!" So, make sure you have documented evidence for the assumptions used in your recommendations, and that they are used consistently across your firm.

The Barclays Equity Gilt Study is one good source of long-term asset class returns to benchmark/check your model assumptions. The table below shows the annualised real (after inflation) returns for various time periods to the end of 2020:

Investment Philosophy and Process

Fund and discretionary managers will typically have a document that outlines their core beliefs and how they implement these beliefs – an 'Investment Philosophy and Process'.

It is a simple idea that advisers can replicate – once you know what you believe (Philosophy) it is relatively straightforward to implement it (Process). Trying to run a process without having the guiding philosophies in place is nigh on impossible and risks delivering inconsistent outcomes. The key for adviser firms is to be able to evidence their beliefs. The importance of costs, the key role that asset allocation plays in long-term returns, and the fact that diversification helps deliver a better risk adjusted return, might feature. As will some comment on active vs passive fund management.

Creating a simple investment philosophy folder that stores these beliefs and critically the evidence for them would be a good first step. This might be updated annually.

It is worth recording examples of how you add value at each of these steps. This can be used in client facing material/reports, for example: the value of running optimised diversified portfolios – to maximise the return for each client's given risk profile; the value of using some passive elements to reduce the overall costs (perhaps in the more efficient markets); the return boost provided by using the right tax wrapper for each asset class to maximise use of income, savings, and gains tax allowances.

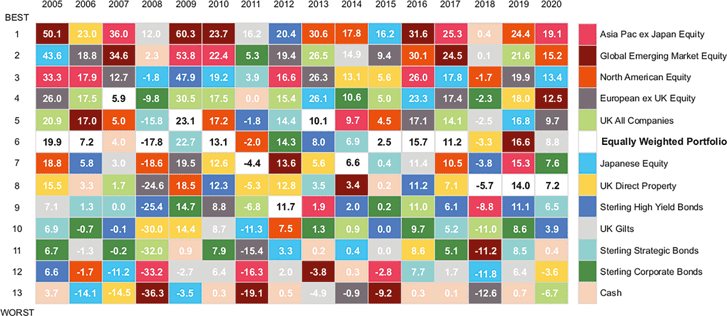

Figure 1. is a simple "quilt" chart that shows how an equally weighted portfolio performs in relation to 12 different IA sectors over 15 years. This is a good piece of evidence for your investment philosophy as well as a good visual sales aid to use in client facing documents.

The Quilt Chart

Source: IMA & FE Analytics as at 31 December each year end

Figures show the median performance rise or fall of each asset grouping per calendar year

Figures are net of charges (other than initial charges)

Past performance is not a reliable indicator of future returns

For authorised adviser use only. No liability is accepted for any errors or omissions in the document. Past performance is not a guide to the future. TCF Investment does not provide financial advice. Investors should seek independent financial advice from a professional if they are in any doubt about making an investment.

To insource or to outsource

One key area that still creates much debate is the decision to insource or outsource investment management.

There is no right answer (other than the need to evidence good outcomes) but there are a couple of important dimensions that will need to be considered: business and investment (summarised below):

Business

- Ownership – there is substantial value in investment management (hence the rise of vertically integrated solutions), so a growing number of advisers wish to own that value and are creating models or extracting revenue from oversight/implementation.

- Value add – firms will have different views on whether they want to have direct input to the investment process (e.g. fund selection) or not.

- Time – if you have resource and skills to undertake the research, implementation, and reporting.

- Capital / ICAAP – going down the route of having discretionary permissions will create substantial complexity and need for greater capital.

Investment

- SAA / risk benchmarks – how do you determine strategic asset allocation or risk benchmarks for your portfolios?

- TAA views – do you have or wish to implement tactical asset allocation views?

- Fund selection – do you want to manage the research process and implementation of client portfolios? Does your Investment Philosophy drive you to passive or active solutions – are these available at the right price in the market?

- Monitoring / Reporting – do you have enough systems and resource to report appropriately, or to gain access to that reporting (platforms play a key role here)? Do you want to be able to explain to clients the details of each portfolio holding?

We have developed several different templates that might help IFAs in their thinking. Please contact us for more details: advisersupport@tcfinvestment.com

Disclaimer

This publication has been produced by TCF Fund managers LLP (TCF). It is provided to UK authorised financial advisers for information purposes only, and TCF makes no express or implied warranty, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included in this publication.

TCF accepts no liability for use of this report and advisers should seek their own specific compliance or other professional advice.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.