The Final Frontier

of automated (ex-post) reviews conquered

In this edition...

- The final frontier of research and due diligence conquered Eric Armstrong, Client Director

- Hours to minutes Eric Armstrong, Client Director

- World Economic and Market Outlook Graham O’Neill, Senior Investment Consultant, RSM.

- Inflation – what to make of the current dynamics Maria Municchi, Fund Manager, Sustainable Multi Asset Fund Range M&G Investments

- Sustainable Investing – advice from an old hand Hugo Thompson, Multi-Asset Investment Specialist HSBC Asset Management

- The biggest changes in ESG investing over the last 10 years Mark Coles, Head of Nationals & Networks Tilney Smith & Williamson

- Don’t try and defy gravity Catriona McInally, Business Development Manager – Investments Prudential

- Sustainable investing – the defining decades Hamish Chamberlayne, Head of Global Sustainable Equities | Portfolio Manager Janus Henderson

- Finding diversification beyond commercial property Shayan Ratnasingam, Investment Manager Liontrust Multi-Asset team

- Looking to alternatives in an uncertain world Chris Forgan, Portfolio Manager Fidelity Multi Asset

- Developing your investment proposition (CIP or CRP) David A Norman (DAN), CEO, TCF Investment

- Intergenerational Financial Planning Gareth Davies, Pension Specialist, Scottish Widows

- Is your online client reporting up to scratch? Natalie Holt, Content Editor, The Lang Cat

- Partnering here to stay as multi-asset solutions grow Antony Champion, Head of Intermediaries, Brewin Dolphin

- How to Capitalise on the Economic Recovery, Including Morningstar’s Portfolio Positioning Leslie Alba, Associate Director, Research Morningstar Investment Management Europe

- Unemployment insurance is back Kesh Thukaram, Co-Founder Best Insurance

Intergenerational Financial Planning

Gareth Davies

Pension Specialist, Scottish Widows

Intergenerational Financial Planning is a commonly used title, but what does it really mean to an individual and a bereaved family at the moment of truth? How can we as an industry bring this important concept to life, and make it real for clients? What are the risks and opportunities that this important area of financial planning presents? For me, telling the story of my late father's pension death benefits hopefully goes a small way towards answering these questions.

"Post Pension Freedom and Choice, the completion and regular review of pension death benefit nomination forms has never been more important. But it is equally important to ensure that, wherever possible, we are also having conversations with the potential eventual inheritors of these benefits."

A few years ago, my father received a terminal cancer diagnosis and passed away at home several weeks later. Although we probably got more time to plan for the end than most of us will get ourselves, it was still an event that nobody can fully prepare you for. The support that we got from the many institutions and organisations that we interacted with during this difficult time varied dramatically, but one positive area that I want to take some time to reflect on is our own industry, and IFAs and pension providers in particular.

As a pension specialist, I make no apologies for using this example to talk about the issues relating to pension plans and nomination forms specifically. Obviously, there are many other examples of financial planning that this overarching concept can apply to and experiences that I could share, but I want to highlight the importance of having these conversations regarding cascade of pension death benefits and in particular completion of nomination forms as early as possible.

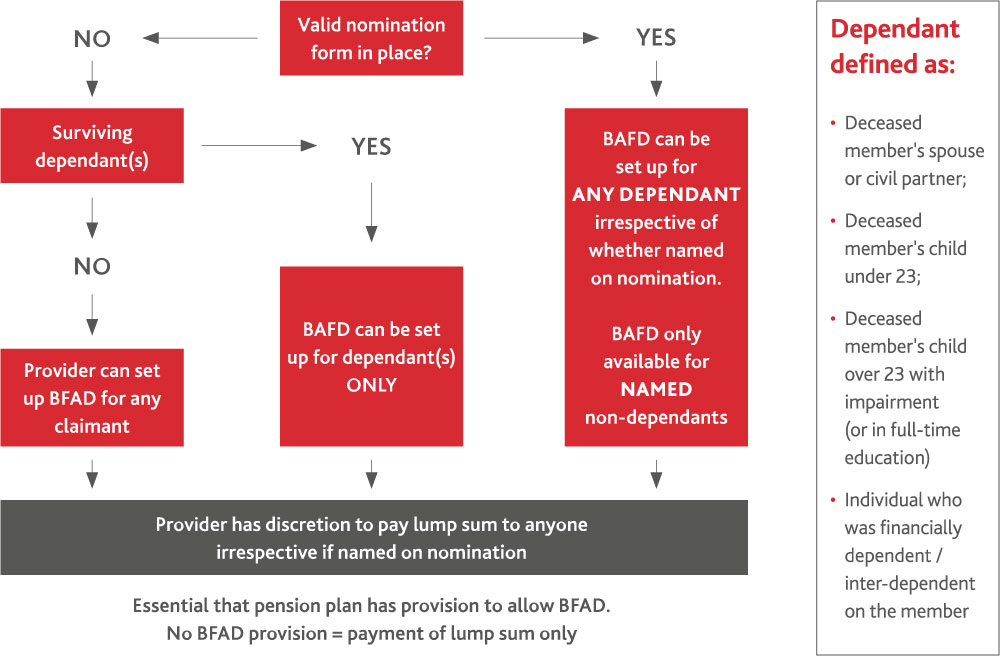

As a brief reminder, prior to Pension Freedom and Choice in 2015, only dependents could receive drawdown following the death of the client. From April 2015, this is now available to anyone. However, it is important to note that if a potential beneficiary is non-dependent, they must be nominated, unless there are no dependents/nominees, in which case Beneficiaries Flexi Access Drawdown can be set up for anyone. The following flowchart provides a useful summary:

How to assess pension death benefit options regarding creation of Beneficiary Flexible Access Drawdown (BFAD)

It is also worth highlighting the limitations of nomination forms. In most instances, benefits will be paid out at the discretion of the scheme administrator/trustee, taking into account all potential beneficiaries (it is possible to make nomination forms a direction on the scheme administrator/trustee, but I won't be covering this in this article). The advantage of this approach is that if the trustees of the pension have discretion over who they pay death benefits to, the benefits are normally free from IHT.

Drawdown beneficiaries can fall into 3 categories:

- Dependant: spouse, child of the member u23, financial dependent etc.

- Nominee: individual nominated by member/scheme.

- Successor: individual nominated by beneficiary/scheme.

It is therefore important that to keep all the Beneficiaries' Flexi Access Drawdown options open on the death of the client, all potential beneficiaries are named on the nomination form.

It is also important to remember that in most instances, nomination forms are not binding instructions on the scheme trustee/administrator and even when these have been completed, they have a duty of care to consider all potential beneficiaries, and not just those named on the nomination form.

This was highlighted to me in the case of my late father's pension following his death. Like many people these days, I come from a blended family – my parents divorced when I was young, and my father remarried a long time ago. As part of his wider inheritance planning, my father's spouse was named as 100% beneficiary on his pension nomination, and we had updated this before he passed away. I had assumed at the time that the product provider would simply proceed on this basis, and I was therefore surprised to be contacted by them following his death to ask if I wished to be considered for payment of his pension benefits. They hadn't just looked at the nomination form and proceed on this basis but had taken the time to understand my late father's wider family, even though I wasn't mentioned anywhere on the pension paperwork.

This really made me stop and think how important it is that we try to have conversations as early as possible with all potential beneficiaries, to ensure that everyone is on the same page following the death of a client. This is even more important in the case of blended families. A family fall out or disagreement following the death of a client can have far reaching consequences.

I also want to take a moment to stress how lucky we are to have a "family" IFA, who has continued to advise my late father's wife and I on the various assets he owned, including the pension, which has continued in place as Beneficiaries Flexi Access Drawdown. He made the whole process simple and straightforward, and ensured that the important taxation benefits of retaining monies in a pension wrapper for as long as possible continued uninterrupted. I worry how many other people will not have the benefit of a trusted "family" adviser to continue the good work after the death of the initial policyholder? Are we all truly planning for the continuation of the good financial plans we have put in place beyond the grave? Are we having conversations now with the eventual inheritors of assets to ensure that they are making informed decisions following the death of a loved one?

Post Pension Freedom and Choice, the completion and regular review of pension death benefit nomination forms has never been more important. But it is equally important to ensure that, wherever possible, we are also having conversations with the potential eventual inheritors of these benefits.

In summary:

- The nomination of beneficiary should be kept up to date.

- This should take account of the legislation around who can receive beneficiary drawdown:

- If there are dependants and/or nominees, the scheme can only set up beneficiary drawdown for those individuals.

- If there are no dependants or nominees, the scheme can set up beneficiary drawdown for anyone.

- Schemes can pay lump sum death benefits to anyone, whether they are named on the nomination form or not.

- Any beneficiary that the member would like to receive beneficiary drawdown that is not a dependant (e.g. adult children) should be nominated.

- This could be on a 98% + 1% + 1% (for spouse/child/child) basis.

For more information, speak to your Business Development Manager or call us on 0345 610 9572.

Gareth Davies is a Pension Specialist for Scottish Widows, specialising in presenting on technical and legislative aspects of both corporate and individual pensions. Gareth has over 30 years’ experience in the life and pensions industry working for major product providers, and over 15 years’ experience as a pensions specialist. Gareth regularly speaks at industry and trade events and he is a Chartered Financial Planner, a Fellow of The Personal Finance Society and also holds the Investment Management Certificate.

Every care has been taken to ensure that this information is correct and in accordance with our understanding of the law and HM Revenue & Customs practice, which may change. However, independent confirmation should be obtained before acting or refraining from acting in reliance upon the information given. Scottish Widows Limited. Registered in England and Wales No. 3196171. Registered office in the United Kingdom at 25 Gresham Street, London EC2V 7HN. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register number 181655.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.