Few places to hide

Sarasin & Partners

In this edition...

- Hours to minutes Editorial team, Synaptic Software Limited

- Synaptic Pathways: the advice research revolution has arrived Eric Armstrong, Client Director, Synaptic Software Limited

- Value for money matters when assessing suitability John Warby, Senior Business Relationship Manager, Synaptic Software Limited

- The road ahead on suitability and disclosure Natalie Holt, Content Editor The Lang Cat

- Developing your investment proposition David A Norman (DAN), CEO TCF Investment

- State of the Nation Ian McKenna, Founder of Financial Technology Research Centre and AdviserSoftware.com FTRC

- Few places to hide Guy Monson, CIO and Senior Partner Sarasin & Partners

- Ensuring the “new normal” is a better normal Ben Lester, Head of Distribution – UK & International Praemium

- Stay the course if you can (but better too early than too late) James Klempster, Deputy Head of the Liontrust Multi-Asset team Liontrust

- Can financial goals be achieved through one fund? Mohneet Dhir, Multi-Asset Product Specialist Vanguard Europe

- Talking Trash: Why it’s not a waste of time Luke Barrs, Head of Fundamental Equity Client Portfolio Management for EMEA & Asia ex-Japan Goldman Sachs Asset Management

- Demand for growth funds rises amid risk-on environment Antony Champion, Head of Intermediaries Brewin Dolphin

- The best of both worlds Ian Jensen-Humphreys, Portfolio Manager Quilter Investors

- Global Sustainable Equity: a renewable, electric and digital future Hamish Chamberlayne, Head of Global Sustainable Equities | Portfolio Manager Janus Henderson

- Four steps to choose an ESG manager Daniel Ryan, Manager Research Analyst Fidelity International

- The path to retirement is changing … are you? Editorial team, Synaptic Software Limited

- Are unregulated investments ever a good idea? Jon Lycett, Business Development Manager RSMR

- Putting the children first Jacqui Gillies, Marketing and Proposition Director Guardian

- Why not Serious Illness Cover? Nick Telfer, Protection Development Manager VitalityLife

The path to retirement is changing … are you?

Editorial team

Synaptic Software Limited

The modern world of retirement is changing. The last 15 years have seen shifts in how people save for, prepare for, and enjoy retirement.

In 15 years from now the number of over 60s will have grown by over a third to more than 20 million. Canada Life's research1 in partnership with forecasting specialists Trajectory, looks at the key trends shaping retirement now, and what this means for financial advice in the future.

How will Financial Services need to adapt to support these new retirement journeys?

Our research finds there are two retirement journeys that will grow significantly over the next 15 years – 'Complex families, complex finances' and 'Late financial bloomers'.

"Although traditional target markets haven't necessarily changed, modern life has, which is creating different opportunities for advisers. An opportunity to rethink client communications and ensure clients are prepared for modern retirement".

Nick Flynn, director, retirement solutions, Canada Life.

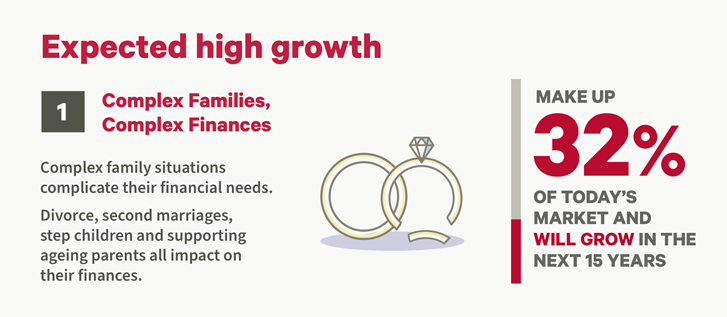

1. Complex Families, Complex Finances

Who are they?

- Average age: Over 65.

- Marital Status: Divorced, separating or cohabiting.

- Housing tenure: Own home or rent.

- Pension status: Historic Defined benefits with an active workplace pension.

This segment accounts for a third of those over 60 and will be the largest group of retirees by 2035. Their wealth and comfort is challenged by the financial implications of a complex family, demands on their finances such as divorce, caring for elderly relatives and second marriages.

Adviser Opportunities

For this group, flexibility and access to their money in retirement is key to support their family in the future. Using tax free cash from a pension may be a good way of clearing debt such as loans or an outstanding mortgage balance.

- Flexible pension A plan is needed that can be adapted to suit your client's changing needs. Ideally low-cost and potentially lets you bring all pension pots together under one simple plan. Clients need to be provided with the flexibility to take a guaranteed income, pension drawdown or a combination of both.

- Protection Can help family members financially if the policyholder dies or becomes seriously ill. If the worst happens, this could help cover children get on the property ladder or pay off an outstanding mortgage.

- Equity Release Could be used for clearing debts such as loans or an outstanding mortgage balance. Over 55s can unlock tax-free cash from their property, with flexibility over the amount they can borrow and whether any repayments are made.

Other opportunities for advisers include optimising digital communication channels, bespoke charging models and a centralised retirement proposition. Read our e-book2 to find out more.

Or, to hear from our experts on this segment watch our CPD qualifying webinar3.

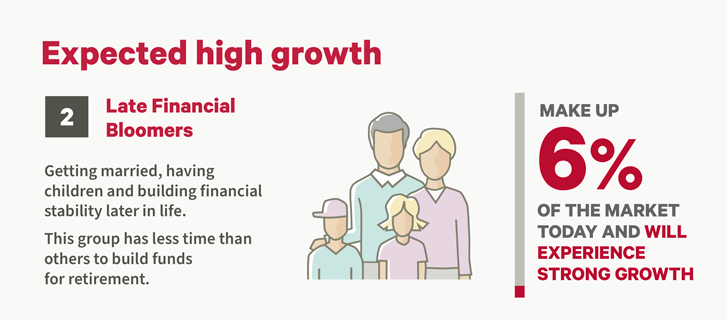

2. Late Financial Bloomers

Who are they?

- Average age: 35+.

- Marital status: Married once, co-habiting or single.

- Housing tenure: Rent or mortgaged home.

- Pension status: Accumulation of retirement wealth compressed by late access to home ownership, marrying and having children later in life.

Currently Late Financial Bloomers are around 6% of adviser's client base but this is due to increase over the next 15 year which presents opportunities for proactive advisers, now and in the future. Late Financial Bloomers are likely to get married, have children and buy property later in life, than previous generations, which may have an impact on their pension pot.

Adviser Opportunities

People in this group are likely to be in employment longer. Reviewing and maximising their contributions to their pensions will be a key consideration for this group.

'I'm amazed that many don't know what they've got in their pension pot. When you explain how it works to them, it is clear that they haven't given it much thought. Understanding the implications of taking money out of your pensions pots is important, and clients need to know which options suit their needs".

Nick Flynn, director, retirement solutions, Canada Life

- Keep the pension pot where it is Your client can defer taking benefits until a later date works for them once they have considered their options.

- Take the pension pot in one go Your client can take their whole pensions pot as a single lump sum (usually only a quarter will be tax free). They will need to plan how this can provide an income for the rest of retirement or have other sources of income.

- Take the pension pot as a lump sum Your client can withdraw lump sum payments from their pension pot at any time, until the money runs out.

- Get a Flexible retirement Income Your client can withdraw regular income from their pension pot. The money left in their pension will remain in an investment fund, so the value of the pension could grow or decrease over time.

- Get a guaranteed income for life The Lifetime Annuity and Scheme Pension use the money saved in your client's pension plan to give them a guaranteed regular income for life. Depending on your client's circumstance, they can choose to provide an income and/ or lump sum after death to a partner or other beneficiaries like children.

- Combine pensions options Your client can choose to access their retirement savings using a combination of the above. They can do this over a set period or until they have used their entire pot. Some pension providers can offer a combination of a guaranteed income for life with a flexible income.

Other opportunities for development include understanding estate planning, inheritance tax implications and getting suitable protection in place.

Read our e-book to find out more[4], or you can watch our CPD Qualifying Webinar[5] to understand how nurturing this group can create opportunities for advisers.

Source:

- Research for Canada Life was conducted in partnership with Trajectory, a strategic futures consultancy. It uses horizon scanning to identify the key trends shaping retirement now and in the future (to 2035), to identify a series of new models of retirement or journeys through later life.

- https://indd.adobe.com/view/d2b0b0af-2309-40fc-9f30-58037d389078

- https://www.canadalife.co.uk/technical-support/webinar-retirement-journeys-complex-families-complex-finances/

- https://indd.adobe.com/view/abca631c-9d14-4ff3-abdb-59b410613b69

- https://www.canadalife.co.uk/technical-support/webinar-nurturing-late-financial-bloomers-to-help-grow-your-business/

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.