Are high quality bonds primed to bloom in 2023?

Connection Magazine Q1 2023

In this edition...

- What we know – and what we don’t Patrick Farrell, Chief Investment Officer and Head of Research - Charles Stanley

- Regime shift: five seismic adjustments taking place in the global economy Azad Zangana, Senior European Economist and Strategist - Schroders

- How to navigate a recession Mike Coop, Morningstar Investment Management - EMEA

- High quality bonds are primed to bloom in 2023 John Pattullo, Co-Head of Global Bonds- Janus Henderson

- Fixed Income - Research Matters Andrew Metcalf, Fixed Income Portfolio Manager - Close Brothers Asset Management

- From 'TINA to 'TANIA'... Bryn Jones, Head of Fixed Income - Rathbones

- The RSMR Broadcast: How impactful is investment management outsourcing? Scott McNiven, MPS Accounts Manager - RSMR

- Hours to minutes Synaptic,

- Benefits of outsourcing and model portfolios Evelyn & Partners,

- DFM Due Diligence – some observations Sean Hawkins, Head of Business Development - M&G Wealth Investments

- 2022 – The death knell for the 60/40 approach to investing? John Husselbee, Head of Multi-Asset - Liontrust

- Why ‘nature positive’ will be as big as net zero Jenn-Hui Tan, Global Head of Stewardship & Sustainable Investing - Fidelity International

- The rise of the female investor Vanessa Eve, Investment Manager - Quilter Cheviot

- Integrate your Centralised Investment Proposition (CIP) with Synaptic Pathways Eric Armstrong, Client Director - Synaptic

- The convergence of regulation in Consumer Duty Eric Armstrong, Client Director, Synaptic

- Tackle Consumer Duty with the new Synaptic integration Alan Lakey , Director - CIExpert & Highclere Financial Services Ltd

The rise of the female investor

Vanessa Eve

Investment Manager - Quilter Cheviot

The rise of the female investor is set to continue according to new research, which poses important considerations for advisers.

The rise of the female investor is set to continue according to new research, which poses important considerations for advisers.

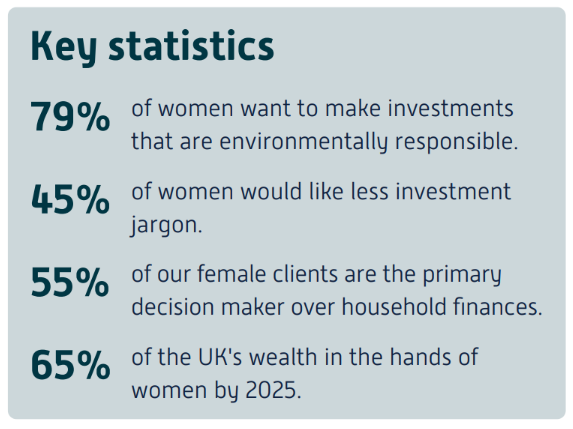

Investment has traditionally been a male-dominated arena, both professionally and among those investing in the markets. We are seeing a change and shifting demographics will see 65% of the UK’s wealth in the hands of women by 2025. This is not just a short-lived fad advisers can simply ignore. Instead, this will impact businesses across the advice space of all sizes. Which is why it is important for advisers to start preparing now.

Understanding female investors

We studied this area in a recent report, by gauging the opinions and perspectives of our female clients.

Crucially, although the majority of our female clients are the primary decision maker over household finances (55%), they are less comfortable with long-term financial decisions. This links to the fact many of our female clients identified gaps in their understanding of investment.

This creates an understandable hesitation to invest.If an investor does not understand risk, they will be reluctant to invest their money.

This can make it difficult to help them achieve their financial goals and could potentially limit their options. This also feeds into the misconception that women are more risk-averse than men.

Indeed, most of our female clients (70%) agree that men’s and women’s attitudes to investment are different. However, when delving deeper, such attitudes are not hugely different. The minority of respondents (14%) report that the difference is significant, with nearly half (44%) regarding them as moderate. These findings reflect the fact there is an unconscious bias in the financial services industry, with women being asked different questions about risk. Other research has found women are more willing to take on risk when given better information – meaning women are more ‘risk-aware’ than necessarily ‘risk-averse’.

Advisers should also understand how attitudes among female investors can differ from men in relation to responsible investment. A WealthiHer survey found 79% of women wanted their investments to be environmentally responsible, versus 65% of men. Responses of 89% and 70%, respectively, were received when asked about socially responsible investment. It is clear female investors put a greater emphasis on such issues, which should be recognised by advisers.

Of course, advisers also need to take into account the other financial differences between men and women. Aside from the obvious ramifications of the gender pay gap, women are more likely to have worked part-time, taken career breaks to have children, or acted as a caregiver. Pay disparity, combined with longer life expectancies, means women will usually need an average of £50,000 more in savings to compensate for retirement income shortfalls.

This has clear repercussions for the role investments will play in a woman’s retirement plan. Of our sample, 64% said they had held their wealth in cash which is not known for its growth properties. Given their smaller pension pots, female investors’ investments will actually need to work harder to achieve greater returns to be comparable to men’s pensions.

"Pay disparity, combined with longer life expectancies,

means women will usually need an average of £50,000

more in savings to compensate for retirement income

shortfalls."

Responding to the rise of female investors

It is important advisers ensure they are giving female investors the appropriate support and advice they need. This involves creating a positive investment experience for women.

Communication is a key part of this. Our research shows nearly half (45%) of clients would like less jargon to promote investment understanding, while the same percentage want help understanding how changes in their personal life impact their finances. This echoes the findings of a 2018 study by Fidelity that found nearly a quarter of women would be more willing to invest if it was made easier to understand. Advice practices set up to cater to a more even split of male and female investors will be better placed to gain new clients.

Advisers are also at risk of losing existing business as men are likely to take a lead over a couple’s financial matters and deal directly with their adviser. Research by UBS found 85% of women will manage day-to-day expenses, but only 19% will share long-term financial decisions with their partner. This can create issues in times of divorce or death (we found 46% of women first engaged with investment after receiving an inheritance). It is not surprising in these circumstances (which are not uncommon due to the fact women live longer than men) that upon discovering a lack of relationship and support, a wife will take her money elsewhere.

It is important for advisers to differentiate their approach between male and female clients. This also should not be restricted to couples and engaging with both partners. More women are putting their careers first, ahead of having families, and becoming successful in their own right. The days of targeting solely men as prospects are long gone.

Get in touch

Transforming women's futures insights report The full report, in which we gathered the responses of thousands of women to better understand their current investment positions, their investing habits and attitudes towards investing, is available to download here:

www.quiltercheviot.com/news-and-views/ women-and-investing/transforming-womens-financial-futures/

Women and investing hub

Explore the key ingredients for successful investing and how we can help you on your investment journey. Visit the women and investing hub at: www.quiltercheviot.com/news-and-views/women-and-investing/

Approver Quilter Cheviot Limited, 28th February 2023.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.