Are high quality bonds primed to bloom in 2023?

Connection Magazine Q1 2023

In this edition...

- What we know – and what we don’t Patrick Farrell, Chief Investment Officer and Head of Research - Charles Stanley

- Regime shift: five seismic adjustments taking place in the global economy Azad Zangana, Senior European Economist and Strategist - Schroders

- How to navigate a recession Mike Coop, Morningstar Investment Management - EMEA

- High quality bonds are primed to bloom in 2023 John Pattullo, Co-Head of Global Bonds- Janus Henderson

- Fixed Income - Research Matters Andrew Metcalf, Fixed Income Portfolio Manager - Close Brothers Asset Management

- From 'TINA to 'TANIA'... Bryn Jones, Head of Fixed Income - Rathbones

- The RSMR Broadcast: How impactful is investment management outsourcing? Scott McNiven, MPS Accounts Manager - RSMR

- Hours to minutes Synaptic,

- Benefits of outsourcing and model portfolios Evelyn & Partners,

- DFM Due Diligence – some observations Sean Hawkins, Head of Business Development - M&G Wealth Investments

- 2022 – The death knell for the 60/40 approach to investing? John Husselbee, Head of Multi-Asset - Liontrust

- Why ‘nature positive’ will be as big as net zero Jenn-Hui Tan, Global Head of Stewardship & Sustainable Investing - Fidelity International

- The rise of the female investor Vanessa Eve, Investment Manager - Quilter Cheviot

- Integrate your Centralised Investment Proposition (CIP) with Synaptic Pathways Eric Armstrong, Client Director - Synaptic

- The convergence of regulation in Consumer Duty Eric Armstrong, Client Director, Synaptic

- Tackle Consumer Duty with the new Synaptic integration Alan Lakey , Director - CIExpert & Highclere Financial Services Ltd

Why ‘nature positive’ will be as big as net zero

Jenn-Hui Tan

Global Head of Stewardship & Sustainable Investing - Fidelity International

With around half of global GDP moderately or highly dependent on nature, it is no surprise that biodiversity is moving up the agenda of companies, policy makers and investors. Global Head of Stewardship & Sustainable Investing Jenn-Hui Tan discusses the risk biodiversity loss poses to investors and outlines what needs to happen to unlock the financing needed to effectively tackle this issue.

With around half of global GDP moderately or highly dependent on nature, it is no surprise that biodiversity is moving up the agenda of companies, policy makers and investors. Global Head of Stewardship & Sustainable Investing Jenn-Hui Tan discusses the risk biodiversity loss poses to investors and outlines what needs to happen to unlock the financing needed to effectively tackle this issue.

The recent UN Biodiversity Conference in Montreal, also referred to as COP15, has helped move the issue of biodiversity up the agenda of companies, policy makers, and investors. The phrase increasingly being used is ‘nature positive’, the idea that the true economic value of nature should be accounted for and that the world should go beyond mere damage limitation. By agreeing a set of rules and standards that encourages nature positive capital allocation, there is an ambitious target of reversing biodiversity loss by 2030 and restoring natural ecosystems by 2050.

This is easier said than done. Biodiversity, which refers to the variety and abundance of life on Earth, is an even tougher nut to crack than climate change. The assessment tools available are also less developed than in other areas of sustainability. For example, investors wanting to compare the climate impact of different projects or portfolios can use a now widely adopted metric called CO2-equivalent to assess emissions of different greenhouse gases using the same scale.

A lack of common standards for biodiversity is problematic

There is no similar benchmark metric for biodiversity. While emissions into the atmosphere contribute to climate change regardless of where they occur, the effects of human interactions with nature differ widely from one location to another. What’s devastating in one place might have minimal impact in another. Each ecosystem has its own unique combination of soils, minerals, water, climatic conditions, and other factors that make it hard to devise metrics that can be broadly applied.

A global disclosure standard based on several complementary metrics is possible and it is encouraging that the International Sustainability Standards Board is planning to add biodiversity to the IFRS sustainability disclosure standards. However, at present, one company might report the number of hectares of land it protects, while a peer in the same industry reports how many species of trees it plants. Working out which is doing more good for nature is a tough ask.

Requiring similar firms to share the same information, so that one investment’s impacts and dependencies on nature can be directly compared against another, would be a significant step towards unlocking the financing needed to tackle the biodiversity threat. So too would aligning standards internationally and, where possible, integrating new rules with existing climate standards to reduce costs and friction. This is for the same planet, after all.

"Around half of global GDP is moderately or highly dependent on nature, according to the World Economic Forum. Either we change our way of life to preserve natural capital, or we deplete it and have to change how we live anyway."

The risk of inaction

Ignoring the issue because it’s complex is not an option either. There are huge risks associated with inaction, most obviously for nature itself but also for businesses and investment portfolios. There are physical risks - many businesses depend on natural processes, such as crop pollination for agriculture. There are transition risks - companies failing to prepare could find themselves on the wrong side of new regulation aimed at ending deforestation or protecting nature. And there are reputational and litigation risks for firms found to be causing harm.

On the international stage, the Taskforce for Nature-related Financial Disclosures (TNFD), modelled on the earlier Taskforce for Climate-related Financial Disclosures (TCFD), is due to be finalised in 2023. TCFD reporting is already mandatory for some activities in the UK and Switzerland and is due to be rolled out in jurisdictions around the world. The same ought to happen with TNFD in time.

Around half of global GDP is moderately or highly dependent on nature, according to the World Economic Forum. Either we change our way of life to preserve natural capital, or we deplete it and have to change how we live anyway. Giving investors tools like the right data they need in order to act on biodiversity is an important step.

Our approach

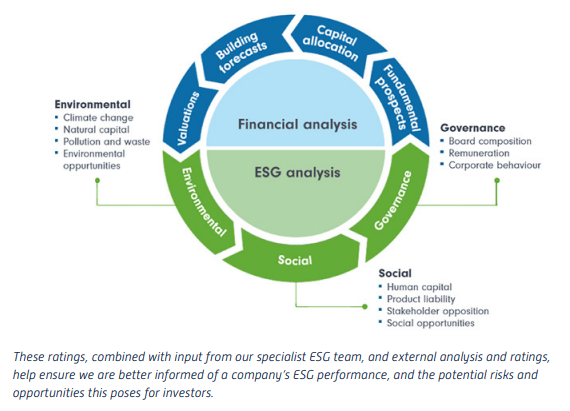

We believe that assessing sustainability is part of fundamental investing, and by integrating it into our investment processes, we can gain a complete view of the companies and markets that we monitor. Through our corporate access, due diligence processes and industry expertise, our investment analysts deliver independent sustainability analysis that is summarised by our proprietary ESG ratings.

Get in touch

www.professionals.fidelity.co.uk/sustainable-investing/our-approach

Important Information:

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. A focus on securities of companies which maintain strong environmental, social and governance (“ESG”) credentials may result in a return that at times compares unfavourably to similar products without such focus. No representation nor warranty is made with respect to the fairness, accuracy or completeness of such credentials. The status of a security’s ESG credentials can change over time. Issued by Financial Administration Services Limited and FIL Pensions Management, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited.

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.