The future is bright… but it will be a bumpy ride

Connection Magazine Q1 2025

In this edition...

- The future is bright for financial advice… but it will be a bumpy ride James Goad, Managing Director - Owen James

- Trump, tariffs, tech, and the rest of the world Fabian Wiesner, Head of Distribution Partnerships - Simplybiz

- Infrastructure: The UK’s untapped goldmine for investors? Katie Sykes, Client Engagement & Marketing Manager - RSMR

- The regulatory landscape for 2025 Sandy McGregor, Director of Policy - Simplybiz

- Can active and passive team up for investment success? Nick Millington, Head of Systematic Index Solutions - Aberdeen Investments

- Why your back-office tech should be invisible Abi Hortin, Implementation Specialist - Plannr Technologies Limited

- 2025 Planning and beyond… Scarlet Musson, Business Development Director - APS Legal Associates

- Marking 10 years of Multi-Asset Income BNY Investments,

- Trump, hitting the ground running Jonathan Griffiths, CFA Investment Product Manager - ebi Portfolios

- Weak UK outlook calls for nuanced approach Caroline Shaw, Portfolio Manager - Fidelity International

- Managing CGT through unitised funds Antony Champion, Managing Director, Head of Intermediaries - RBC Brewin Dolphin

- Expanding Decumulation Capabilities in Pathways Seb Marshall, Product Manager - Synaptic

- DFM due diligence and the role of financial strength consideration Matt Ward, Communications Director - AKG Financial Analytics Ltd

- Benefits of Investing on Global Listed Infrastructure Giuseppe Corona, Head of Listed Real Assets - HSBC Asset Management

- Taking stock of the new world order Ariel Bazalel, Investment Manager - Jupiter Strategic Bond Fund

Weak UK outlook calls for nuanced approach

Caroline Shaw

Portfolio Manager - Fidelity International

The UK economy has been in the news for the wrong reasons in recent weeks. UK growth has petered out after a promising start to 2024 and rising government bond yields have provoked comparisons with Liz Truss’s disastrous mini budget in 2022.

The UK economy has been in the news for the wrong reasons in recent weeks. UK growth has petered out after a promising start to 2024 and rising government bond yields have provoked comparisons with Liz Truss’s disastrous mini budget in 2022.

There is no doubt that the outlook for the UK has deteriorated. We are still waiting for all the data, but it looks like GDP growth will come in at zero over the second half of 2024, much weaker than many initially thought. We do expect a minor recovery to 1% growth in 2025, however this is well below the forecasts of the Bank of England and the OBR. The drivers of this growth are likely to remain the same: better consumption due to improving real disposable income growth and an expected drawdown of elevated excess savings. A lower Bank of England base rate may also help to reinvigorate capex and housing investment, but there’s likely a low ceiling to any recovery given the ongoing weak sentiment.

Similarly, the labour market is also worsening. Multiple surveys indicate employment is declining and we expect this to continue in 2025 as layoffs increase in response to compressed margins amid weak demand and National Insurance tax increases.

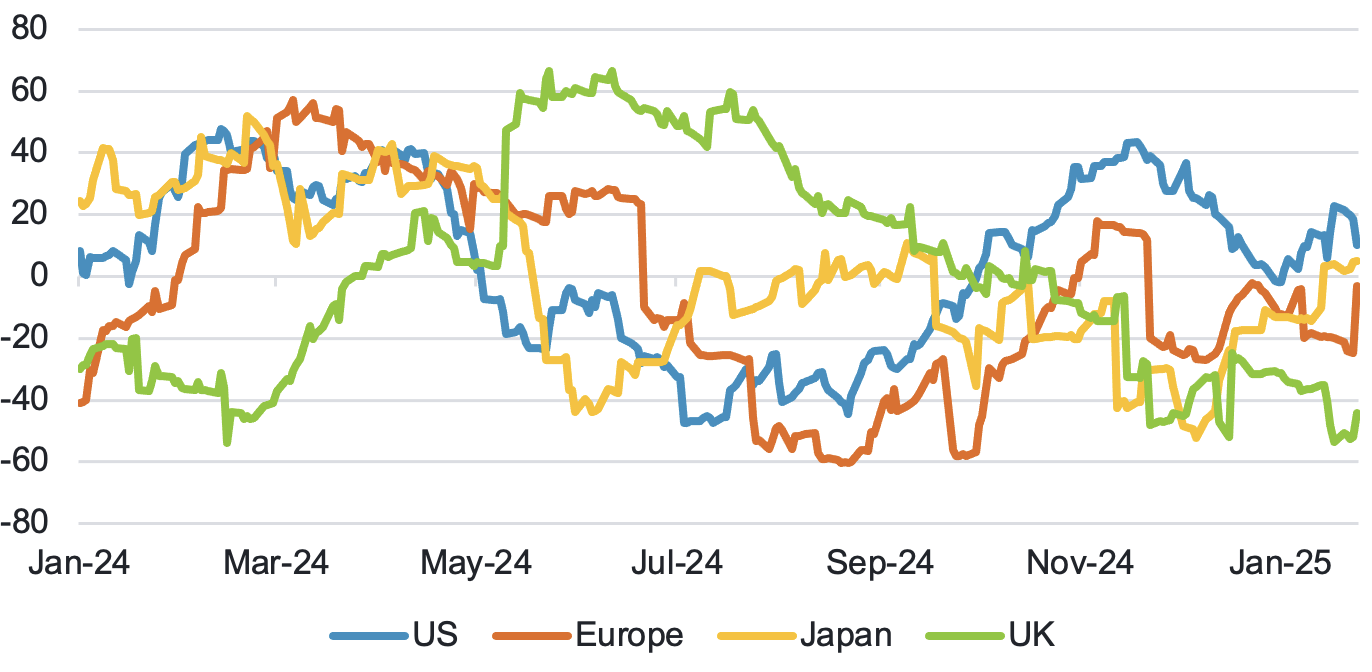

UK’s positive start to 2024 fizzles out

Citi Economic Surprise indices

Source: LSEG Datastream, Fidelity International, February 2025

Inflation remains relatively high, despite a welcome downside surprise in December. However, VAT on private school fees and energy price rises will likely maintain upwards pressure on inflation for the time being.

Finally, the UK’s fiscal situation, while not as bad as the mini budget debacle of 2022, also looks unenviable. Last year’s budget proved more expansionary than expected, featuring higher spending, taxes, and borrowing. Government debt is forecast to rise over the coming years, and meeting the fiscal rule of falling debt by the end of the current parliament relies on optimistic growth assumptions (2% for 2025 and above 1.5% throughout the forecast horizon).

Many have pointed to the UK’s twin deficit dynamics (fiscal and current account) as an area for concern, which makes it more sensitive to global interest rates. Indeed, the recent rise in yields has essentially eliminated the government’s fiscal headroom due to rising borrowing costs.

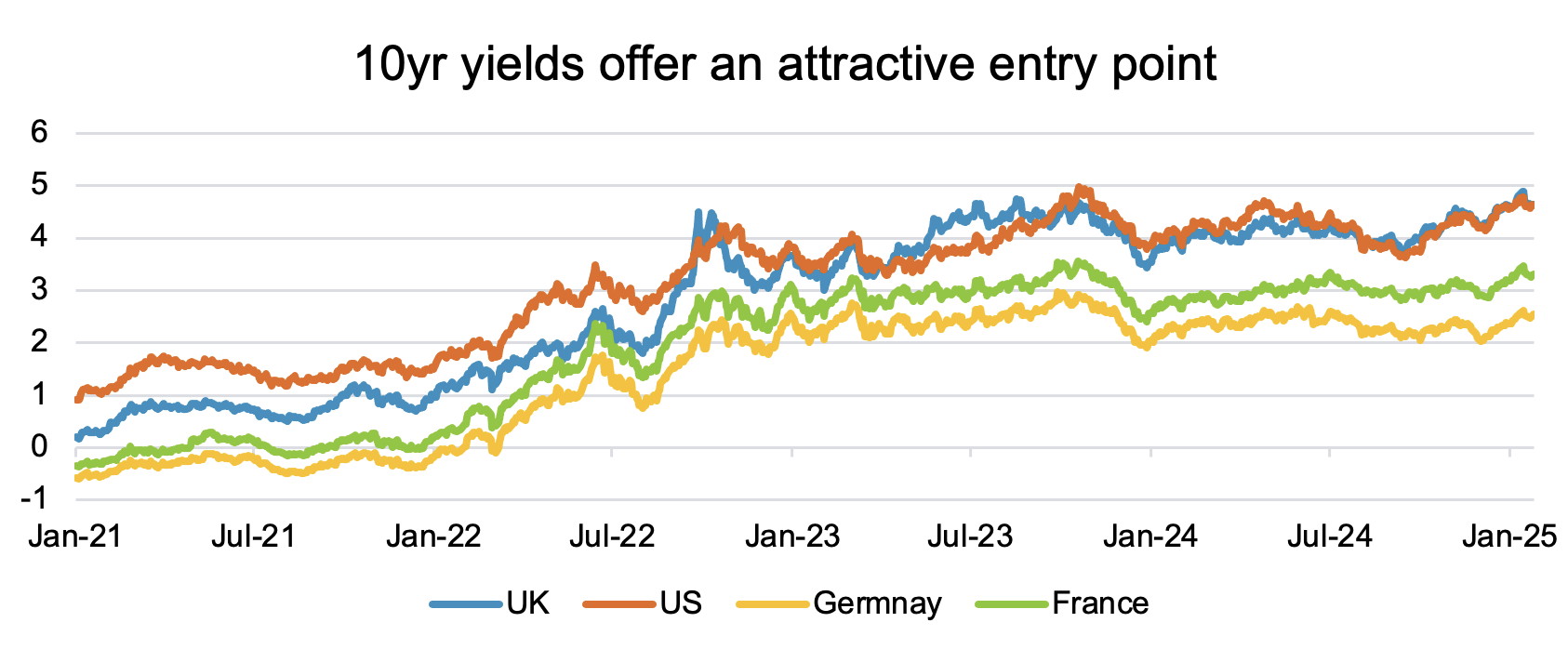

Yields on UK Gilts are attractive

Given the poor macro backdrop, we believe UK government bonds present an attractive proposition, and we have been adding to our Gilts position for the last few months. The recent rise in yields was largely caused by global rates moves rather than a significant reappraisal of the UK’s fiscal situation and presents investors with an attractive entry point. The yield on 10-year Gilts now sits at around 4.6%, similar to that of US Treasuries. However, the UK has a notably worse growth and labour market outlook than the US. Markets are pricing in around three rate cuts from the BOE this year and we believe the eventual total could be more than that, which would be an additional tailwind for Gilts.

UK equities offer stock picking opportunities

Our outlook for UK equities is more mixed. The UK macro environment is not encouraging. However, there are a few silver linings: valuations remain attractive, the BOE cutting rates should help growth, and the UK is relatively insulated from the threat of US tariffs. We had been overweight in the first part of 2024 in reflection of the brighter economic news at the time, but the 2024 autumn budget was not as pro-growth as we had hoped, causing us to reduce our position to neutral overall.

However, we have identified two UK active managers that we believe have excellent potential to add alpha through stock selection. As such, we have positions in UK equity funds from both Artemis and Polar Capital as well as a short position in the FTSE 250 index. This reduces our exposure to UK equity market movements while the outlook is poor while retaining our ability to capture alpha from managers that we believe will perform strongly.

We like the distinct investment process that the portfolio managers follow at Polar Capital. Their clear philosophy and investing discipline ensure consistency in the types of company they select. We believe the fund is a good option for active small-and mid-cap UK equity exposure. Meanwhile, the Artemis UK Select fund is a concentrated multi-cap best ideas fund run by experienced portfolio manager Ed Legget, who has an exceptional track record of managing UK equity portfolios. Despite returning c.50% over the last 2 years, the fund still trades at a discount to the market. This indicates that the fund could offer downside protection versus the broader UK market if sentiment were to sour and could even experience stronger returns if sentiment improves and multiples expand.

We will continue to monitor the UK for changes to the macroeconomic backdrop and search for the best top-down and bottom-up opportunities to add alpha.

Learn more about Fidelity’s Multi Asset solutions

Get in touch:

www.professionals.fidelity.co.uk

Important Information: This information is for investment professionals only and should not be relied upon by private investors. The value of investments and the income from them can go down as well as up and clients may get back less than they invest. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. The investment policy of the Fidelity Multi Asset funds mean they invest mainly in units in collective investment schemes. Fidelity’s Multi Asset funds use financial derivative instruments for investment purposes, which may expose the fund to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in emerging markets can also be more volatile than other more developed markets. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates rise and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only. Issued by FIL Pensions Management, authorised and regulated by the Financial Conduct Authority. Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document (KIID), current annual and semiannual reports free of charge on request by calling 0800 368 1732. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited.

UKM0225/400023/SSO/NA

Sign up for updates

Keep up to speed with everything you need to know each quarter, by email or post.